House Republican plan to repeal the ACA will hurt Ohio

March 10, 2017

House Republican plan to repeal the ACA will hurt Ohio

March 10, 2017

Ohio may be forced to end Medicaid expansion within a few years

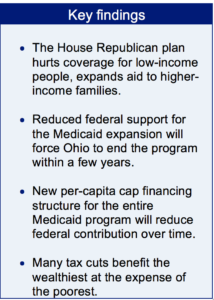

Key Findings

- The House Republican plan hurts coverage for low-income people, expands aid to higher-income families.

- Reduced federal support for the Medicaid expansion will force Ohio to end the program within a few years.

- New per-capita cap financing structure for the entire Medicaid program will reduce federal contribution over time.

- Many tax cuts benefit the wealthiest at the expense of the poorest.

Contact Wendy Patton 614.221.4505 Download report Executive summary Press release

The House Republican proposal to “repeal and replace” the ACA will, over time, force Ohio to eliminate the Medicaid expansion, which will cause hundreds of thousands of low-income Ohioans to become uninsured. It will also dramatically reduce the value of the tax credits people receive to help buy insurance now on the private market. Many Ohioans will get less help. Most Ohioans helped by the ACA gained health insurance through Medicaid expansion, which the House Republican plan repeals. The people who would become uninsured, or find their coverage much more expensive, are from low-income families with workers in Ohio’s largest occupational groups, such as food service and table waiting, retail, home health, and cleaning and janitorial.

The House Republican proposal to “repeal and replace” the ACA will, over time, force Ohio to eliminate the Medicaid expansion, which will cause hundreds of thousands of low-income Ohioans to become uninsured. It will also dramatically reduce the value of the tax credits people receive to help buy insurance now on the private market. Many Ohioans will get less help. Most Ohioans helped by the ACA gained health insurance through Medicaid expansion, which the House Republican plan repeals. The people who would become uninsured, or find their coverage much more expensive, are from low-income families with workers in Ohio’s largest occupational groups, such as food service and table waiting, retail, home health, and cleaning and janitorial.This issue brief covers changes to Medicaid and the insurance subsidy in the exchanges. The GOP repeal plan included many additional changes. They will be covered in forthcoming briefs.

Short-term consequences of the House bill (over the next 5 years):

- The House bill dramatically lowers the federal matching rate for the expansion group. As a result, about 700,000 Ohioans — mostly low-income workers — will lose coverage through the Medicaid expansion.

- The Kasich administration estimates it would cost the state $1.5 billion a year to continue covering the population covered by Medicaid expansion. Other parts of the Republican plan drive costs even higher. [1]

- The Medicaid program itself is restructured from a financial partnership between the federal government and states based on needs to a set rate per-enrollee based on 2016 demographics and cost.

- Many of the 212,000 Ohioans of low and moderate income who purchase insurance in the federal marketplace will face higher costs with elimination of subsidies for out-of-pocket expenses and changes to tax credits.

- Older Ohioans, especially those of low and moderate income, will face increased insurance premium costs as the ACA repeal lifts caps on what insurers can charge as people age.

- Women who use Planned Parenthood clinics may find them shuttered as the GOP plan eliminates federal funding for providers who include abortion in their services.

- Women who purchase insurance through the federal exchange will not have access to health plans that include coverage of abortion.

- Changes to the financing structure of the Medicaid program — which covers 3 million Ohioans, a quarter of the population — would dramatically reduce federal support over time, which would force Ohio to reduce eligibility for coverage and benefits among seniors, kids, and people with disabilities.

- As Ohio ages and cost of caring for the elderly rise, Ohio would face penalties and cuts in federal funds. The state may face hard choices, such as whether to reduce care for costly yet growing segments of the population, like seniors.

- Ohio has raised $99 million from the ACA’s Prevention and Public Health Fund since 2010,[2] which is repealed in the GOP plan.

The ACA allowed low-income workers earning up to 138 percent of the federal poverty level (about $16,000 a year for an individual) to become eligible for Medicaid coverage. This provides health insurance for people working in Ohio’s largest occupational groups, like retail, food service, home health, janitors and cleaners. Employers rarely offer these workers health benefits.

The Republican plan to repeal the ACA eliminates Medicaid expansion on December 31, 2019. Those who are enrolled up to and on that date may remain in the program until they leave. If they separate from the program for longer than a month, they are considered “out.” If they re-enroll, the Medicaid expansion’s federal “match” rate is eliminated (90 cents for each $1 spent on their care). This will create a much greater cost on states if they continue to provide health coverage for these people, leading many to question if such coverage will continue.

The Kasich Administration projects the repeal of Medicaid expansion would cost the state $1.5 billion in order to continue coverage for the expansion population.[3]

On March 6, 2017, Senator Robert Portman joined with Shelley Moore Capito (R-WV), Cory Gardner (R-CO) and Lisa Murkowski (R-AK) in a letter to Senate Majority Leader Mitch McConnell. Portman pointed out: “The Medicaid population includes a wide range of beneficiaries, many of which cycle on and off Medicaid due to frequent changes in income, family situations, and living environments.”[4] In effect, repeal will be implemented through the cycling mentioned by the senators. As people leave the program, they will not be allowed back in – unless the state accepts them into the regular Medicaid program under new rules that will reduce federal share of Medicaid and make it less likely the state will provide coverage.

Changes to the Medicaid Program

Medicaid is the largest health insurer in Ohio, covering more than 3 million people – a quarter of Ohio’s population. The Republican plan would dramatically change the financing structure of the program, which will reduce federal funding over time and lead to a thinning of coverage.

Currently, the federal government pays a fixed percentage of the cost of covering each Medicaid enrollee. In Ohio, that share is about 62 cents of each $1 of Medicaid spending. If your income is under the threshold of eligibility, you get health insurance through Medicaid, and the federal government pays a predictable share of the cost of your care. If a recession hits, or an epidemic, the partnership between the state and the federal government work together to protect health of the people and the health care system.

The new GOP plan proposes a “per-capita cap” mechanism. That plan would cap how much the federal government gives each state per Medicaid enrollee, based on how much the state spent in 2016. Federal funding for every Medicaid beneficiary would rise with the medical component of the Consumer Price Index, or the price of medical care, but not with changing circumstances or demographics. The federal share can grow with enrollment if more people sign up for Medicaid, as they do during a recession. However, it does not grow if the cost of care for Medicaid patients increases, as it does in an epidemic or when a population ages. The federal share won’t adjust if states want to offer new benefits or increase payments to health care providers.

For a state like Ohio, where the population is aging rapidly, that could cause harm. In 2010, 19.8 percent of Ohio’s population was 60 or older. The Scripps Center for Gerontology estimates that number will climb to 25.2 percent by 2020 and 29.3 percent by 2030.[5] Health care needs and costs rise with age. As seniors make up a larger share of the population, costs per beneficiary will rise. In Ohio, the elderly, blind and disabled make up 29 percent of total Medicaid spending, but they account for just 9 percent of total enrollment.[6] As that enrollment rises as the population ages, controlling costs pegged to 2016 demographics will become more difficult.

This is compounded by the penalty for exceeding costs contained in the language of the Republican plan. The summary of the plan, put out by the House Energy and Commerce Committee, describes the new financing mechanism as follows:[7]

[It] would use each State’s spending in FY2016 as the base year to set targeted spending for each enrollee category (elderly, blind and disabled, children, non-expansion adults, and expansion adults) in FY2019 and subsequent years for that State. Each State’s targeted spending amount would increase by the percentage increase in the medical care component of the consumer price index for all urban consumers from September 2019 to September of the next fiscal year. Starting in FY2020, any State with spending higher than their specified targeted aggregate amount would receive reductions to their Medicaid funding for the following fiscal year.[8]The proposed per-capita cap structure, combined with the penalty, could cause states to drop costly populations, like seniors or disabled people, as a result of fiscal concerns.

Federal policymakers use block grant or per-capita cap system to reduce federal spending over time. This was the case with welfare reform in the 1990s, which resulted in a long-term reduction of that program, eroded by inflation and now used by many states to backfill for state resources instead of supporting needy families. In 1979 Aid to Families with Dependent Children served 82 out of 100 eligible poor families. Today, it serves just 23 out of every 100 eligible families.[9] We can expect the same effect in block granting Medicaid. The Republican plans dramatically changes the structure of Medicaid from a flexible funding partnership between the states and federal government. Currently, Medicaid is considered “mandatory” in congressional terms. This means it is protected from annual federal budget debates. The Republican plan would make Medicaid “discretionary” so it would be based on a less flexible structure and exposed to legislative scrutiny and annual budget changes. Further cuts in the program become easier.

Changes in insurance tax credits and subsidies

Federal aid to help families and people buy private insurance is not repealed by the Republican plan, but it is changed. Under the House Republican plan, families above the Medicaid eligibility threshold will get less help to purchase in the marketplace, while those with higher incomes will get more help.

The mandate that people participate in health care coverage is repealed, as are the penalties for not participating. The plan uses a new stick to encourage people to buy coverage. People who allow their insurance coverage to lapse can buy insurance again, but their insurer will charge a flat, 30 percent late-enrollment surcharge if the lapse in coverage is greater than 63 days. The surcharge will apply to everyone, regardless of health status, and will continue for 12 months, when it will cease.[10]

The bill would offer tax credits, refundable in advance, to people with incomes below $75,000.

The current, income-based premium subsidies would be replaced by age-based subsidies. Under the ACA, subsidies to help individual buyers afford premiums and (for poorer households) subsidies to help pay out-of-pocket costs (deductibles and co-pays) were based on household income. The proposed Republican plan will base them on the buyer’s age, instead, with older buyers receiving more help than younger. The tax credits are set at one national rate, without regard for regional disparities in cost:

- $2,000 for an individual under 30,

- $2,500 for 30 to 39,

- $3,000 for 40 to 49;

- $3,500 for 50 to 59, and

- $4,000 for 60 and over.

The ACA’s subsidies that helped people of low income with the cost of out-of-pocket expenses are eliminated in the Republican plan. The subsidies are significant for low-income people and families:

- In 2016, people making between 100 – 150 percent of poverty (less than $20,000 a year for an individual) enrolled in a silver plan on healthcare.gov received cost-sharing assistance worth $1,440;

- those with incomes up to $23,760 (between 150 – 200 percent of poverty) received $1,068 on average; and

- those with incomes between 200 – 250 percent of poverty (23,760 to $29,700) received $144 on average.

- In Scioto County, in the Appalachian region of southern Ohio, people of low income, earning $20,000 a year, of all age groups, do better under the ACA than under the Republican plan. For example, a 27-year-old would get $440 a year less under the Republican plan than under the ACA; a 40-year-old would get $180 less and a 60-year-old would get $3,830 less.

- The Republican plan provides higher tax credits for young and middle-aged people earning $20,000 in urban Cuyahoga County, but not nearly enough to offset the loss of the ACA’s additional subsidies for out of pocket expenses.

- At $30,000 a year, all 60-year-olds fare worse under the Republican plan: in an urban county (Cuyahoga), a rural county (Crawford), a suburban/exurban county (Greene) and an Appalachian County (Scioto).

- At $40,000 a year, a 60-year-old loses $3,160 a year in rural Crawford County but gains $1,200 in urban Cuyahoga County.

- Between $50,000 a year and $100,000 a year, all age groups can access tax credits for health care under the Republican plan; they could not under the ACA.

“Current law limits the cost of the most generous plan for older Americans to three times the cost of the least generous plan for younger Americans. The true cost of care is 4.8-to-one, according to health economists. This provision loosens the ratio to five-to-one.”[13]The analysis by the Kaiser Family Foundation demonstrates that everyone over 60 making $30,000 a year or less in Ohio will pay more, on average, under the Republican plan than under the ACA. This has to do with the change in tax credits but also to the new rules which allow seniors to be charged more for their insurance. New aid to the middle class helps some seniors with this bump – largely because the ACA did not provide coverage in these income ranges.[14]

Women – The GOP plan defunds Planned Parenthood: No federal funding can be made, either directly or indirectly, by Medicaid to a healthcare organization that “provides for abortions,” other than those done in cases of rape or incest or to save the life of the mother. That’s Planned Parenthood. (Planned Parenthood doesn’t use federal funds to pay for abortions. That is already against the law.)

The measure forbids spending federal tax subsidies on health plans that include coverage of abortion. This would shrink access to insurance-covered abortions, or even lead to insurers dropping abortion coverage from their plans. [15]

Middle- and upper-income - Americans higher up the income scale would be eligible for subsidies to help them buy health insurance. The law would allow people to save more money each year in tax-free health savings and flexible spending accounts — tax-favored savings accounts typically used by high-income employees of large employers.[16] More middle-income people and families would be eligible for tax credits to help them buy health coverage. The elimination of several taxes will only benefit people of high incomes.

Other benefits that accrue mostly to the wealthy include repeal of:[17]

- The delay of the “Cadillac” insurance plan tax;

- The prohibition against paying for over-the-counter medications with tax subsidized funds from health and medical savings or reimbursement accounts;

- The ACA’s increase in the penalty for the use of health and medical savings and related accounts for non-medical purposes;

- The $2,500 limit on contributions to flexible spending accounts;

- The medical device excise tax;

- The increase in the level of medical expenses that must be incurred to claim a tax deduction from the federal income tax, reducing the level back from 10 percent to 7.5 percent;

- The repeal of the ACA’s Medicare 0.9 percent tax surcharge on taxpayers with incomes exceeding $200,000 ($250,000 for joint filers).

The legislation does not repeal the ACA’s insurance reforms, such as the ACA’s requirements that health plans. It will continue to:

- cover preexisting conditions;

- guarantee availability and renewability of coverage;

- cover adult children up to age 26; and

- cap out-of-pocket expenditures.

- health status underwriting;

- lifetime and annual limits; and

- discrimination on the basis of race, nationality, disability, age, or sex.

The House Republican plan repeals the ACA and replaces it with a program that shifts costs to states and provides less assistance to people with low incomes. It expands aid to middle-income families and gives tax breaks to the wealthy, but reduces aid to low-income families. It will be particularly hard on the lowest income, oldest people among this group. In the short-term in Ohio hundreds of thousands will become uninsured because of the loss of Medicaid expansion and subsidies to buy health insurance on the exchanges.

In the long run, the Republican plan will hurt state Medicaid programs as federal funding is reduced under the per-capita cap financing structure. The Republican plan will particularly harm Ohio. The state has an aging population with many health problems. Ohio suffers from a widespread drug epidemic. The infant mortality rate in some Ohio cities is higher than the rate in some underdeveloped nation. Our health care costs may rise because our needs are high, and growing. Ohio’s median income is below the national average and the state has a huge, low-wage labor market. Our 12 largest job groups leave a family of three in or close to poverty. The people who work in these jobs are the ones who will be hurt the most by the Republican plan.

The House Republican plan threatens too many. The people of the state of Ohio have been helped by the Affordable Care Act. Too many of us will be hurt by the repeal under the new Republican plan.

[1] Catherine Candisky, “Kasich, Tiberi, Jordan differ on GOP health-care plan removing thousands of Ohioans from coverage” The Columbus Dispatch, March 7, 2017 at http://www.dispatch.com/news/20170307/kasich-tiberi-jordan-differ-on-gop-health-care-plan-removing-thousands-of-ohioans-from-coverage. See also Center on budget and Policy Priorities at http://www.cbpp.org/research/health/house-republican-proposals-to-radically-overhaul-medicaid-would-shift-costs-risks-to

[2] Ohio Public Health Association, March 1, 2017 at https://ohiopha.org/tag/fund/

[3] Candisky, Op.Cit. at http://www.dispatch.com/news/20170307/kasich-tiberi-jordan-differ-on-gop-health-care-plan-removing-thousands-of-ohioans-from-coverage

[4] Senator Rob Portman web page at http://www.portman.senate.gov/public/index.cfm?p=press-releases&id=C6D96A68-A891-4BA1-8AD2-1CE166E0F8EB

[5] Scripps Center for Gerontology, Miami University at http://www.ohio-population.org/documents/ohios-population-state-by-age-groups-1990-2050/

[6] Health Policy Institute of Ohio, “Medicaid Basics, 2015” at http://www.healthpolicyohio.org/wp-content/uploads/2016/03/MedicaidBasics_2015_Final.pdf

[7] House Energy and Commerce Committee, Section by Section Summary at https://energycommerce.house.gov/sites/republicans.energycommerce.house.gov/files/documents/Section-by-Section%20Summary_Final_.pdf

[8]House Energy and Commerce Committee, Section by Section Summary, Op.Cit. at https://energycommerce.house.gov/sites/republicans.energycommerce.house.gov/files/documents/Section-by-Section%20Summary_Final_.pdf

[9] Center on Budget and Policy Priorities, August, 2016. “Chartbook: TANF at 20” at https://webpoolblu2a04.infra.lync.com/Scheduler/

[10]House Energy and Commerce Committee, Section by Section Summary, Op.Cit. at https://energycommerce.house.gov/sites/republicans.energycommerce.house.gov/files/documents/Section-by-Section%20Summary_Final_.pdf

[11] Timothy Jost, “Examining The House Republican ACA Repeal And Replace Legislation,” Health Affairs blog, March 7, 2017 at http://healthaffairs.org/blog/2017/03/07/examining-the-house-republican-aca-repeal-and-replace-legislation/

[12] Kaiser Family Foundation at http://kff.org/health-reform/issue-brief/how-affordable-care-act-repeal-and-replace-plans-might-shift-health-insurance-tax-credits/

[13]House Energy and Commerce Committee, Section by Section Summary, Op.Cit. at https://energycommerce.house.gov/sites/republicans.energycommerce.house.gov/files/documents/Section-by-Section%20Summary_Final_.pdf

[14] Kaiser Family Foundation. Tax Credits under the Affordable Care Act vs. the American Health Care Act: An Interactive Map, March 7, 2017 at http://kaiserf.am/2naqGyQ

[15] House Ways and Means Committee, Summary at https://waysandmeans.house.gov/wp-content/uploads/2017/03/03.06.17-Section-by-Section.pdf

[16]Margo Sanger-Katz, “G.O.P. Repeal Bill Would Cut Funding for Poor and Taxes on Rich,” New York Times, March 6, 2017 at http://nyti.ms/2lXpBte

[17] Timothy Jost, Op.Cit. at http://healthaffairs.org/blog/2017/03/07/examining-the-house-republican-aca-repeal-and-replace-legislation/

Sources

[1] Catherine Candisky, “Kasich, Tiberi, Jordan differ on GOP health-care plan removing thousands of Ohioans from coverage” The Columbus Dispatch, March 7, 2017 at http://www.dispatch.com/news/20170307/kasich-tiberi-jordan-differ-on-gop-health-care-plan-removing-thousands-of-ohioans-from-coverage. See also Center on budget and Policy Priorities at http://www.cbpp.org/research/health/house-republican-proposals-to-radically-overhaul-medicaid-would-shift-costs-risks-to

[2] Ohio Public Health Association, March 1, 2017 at https://ohiopha.org/tag/fund/

[3] Candisky, Op.Cit. at http://www.dispatch.com/news/20170307/kasich-tiberi-jordan-differ-on-gop-health-care-plan-removing-thousands-of-ohioans-from-coverage

[4] Senator Rob Portman web page at http://www.portman.senate.gov/public/index.cfm?p=press-releases&id=C6D96A68-A891-4BA1-8AD2-1CE166E0F8EB

[5] Scripps Center for Gerontology, Miami University at http://www.ohio-population.org/documents/ohios-population-state-by-age-groups-1990-2050/

[6] Health Policy Institute of Ohio, “Medicaid Basics, 2015” at http://www.healthpolicyohio.org/wp-content/uploads/2016/03/MedicaidBasics_2015_Final.pdf

[7] House Energy and Commerce Committee, Section by Section Summary at https://energycommerce.house.gov/sites/republicans.energycommerce.house.gov/files/documents/Section-by-Section%20Summary_Final_.pdf

[8] House Energy and Commerce Committee, Section by Section Summary, Op.Cit. at https://energycommerce.house.gov/sites/republicans.energycommerce.house.gov/files/documents/Section-by-Section%20Summary_Final_.pdf

[9] Center on Budget and Policy Priorities, August, 2016. “Chartbook: TANF at 20” at https://webpoolblu2a04.infra.lync.com/Scheduler/

[10] House Energy and Commerce Committee, Section by Section Summary, Op.Cit. at https://energycommerce.house.gov/sites/republicans.energycommerce.house.gov/files/documents/Section-by-Section%20Summary_Final_.pdf

[11] Timothy Jost, “Examining The House Republican ACA Repeal And Replace Legislation,” Health Affairs blog, March 7, 2017 at http://healthaffairs.org/blog/2017/03/07/examining-the-house-republican-aca-repeal-and-replace-legislation/

[12] Kaiser Family Foundation at http://kff.org/health-reform/issue-brief/how-affordable-care-act-repeal-and-replace-plans-might-shift-health-insurance-tax-credits/

[13] House Energy and Commerce Committee, Section by Section Summary, Op.Cit. at https://energycommerce.house.gov/sites/republicans.energycommerce.house.gov/files/documents/Section-by-Section%20Summary_Final_.pdf

[14] Kaiser Family Foundation. Tax Credits under the Affordable Care Act vs. the American Health Care Act: An Interactive Map, March 7, 2017 at http://kaiserf.am/2naqGyQ

[15] House Ways and Means Committee, Summary at https://waysandmeans.house.gov/wp-content/uploads/2017/03/03.06.17-Section-by-Section.pdf

[16] Margo Sanger-Katz, “G.O.P. Repeal Bill Would Cut Funding for Poor and Taxes on Rich,” New York Times, March 6, 2017 at http://nyti.ms/2lXpBte

[17] Timothy Jost, Op.Cit. at http://healthaffairs.org/blog/2017/03/07/examining-the-house-republican-aca-repeal-and-replace-legislation/

Photo Gallery

1 of 22