Kasich tax proposal would skew tax system further in favor of Ohio's affluent

February 10, 2015

Kasich tax proposal would skew tax system further in favor of Ohio's affluent

February 10, 2015

Contact: Zach Schiller, 216.361.9801

Income tax cuts would further contribute to inequality in Ohio

The Kasich administration proposal to cut income taxes and expand sales and other taxes would produce big tax cuts for Ohio’s most affluent residents, while increasing taxes on lower- and moderate-income families.

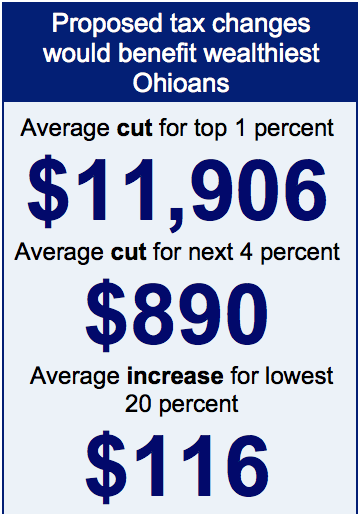

The Kasich administration proposal to cut income taxes and expand sales and other taxes would produce big tax cuts for Ohio’s most affluent residents, while increasing taxes on lower- and moderate-income families.The proposal would provide an $11,906 annual tax cut on average to taxpayers in the top 1 percent of the income spectrum, who made more than $388,000 in 2014. The bottom three-fifths of taxpayers as a group, making less than $58,000 a year, would see increases in state and local taxes. Those in the bottom fifth, making less than $20,000 last year, would see an increase of $116 on average. Even excluding changes in tobacco taxes in Gov. Kasich’s proposal, taxpayers making less than $37,000 a year – those in the bottom two-fifths of the income spectrum – on average would see no benefit from the plan.

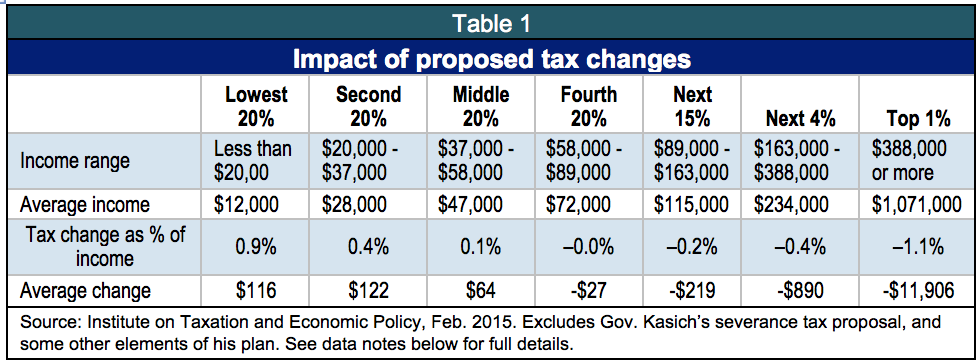

Those are the results of an analysis by the Institute on Taxation and Economic Policy, a Washington, D.C.-based research group that has a sophisticated model of the tax system, for Policy Matters Ohio. Table 1 provides the breakdown of the overall impact of the changes proposed by the Kasich administration, excluding the governor’s severance tax plan.[1]

Income-tax cuts will flow heavily to the most affluent, further increasing inequality in Ohio while doing little for our economy. By contrast, the increase in the sales-tax rate and most of the other proposed tax increases will fall more heavily on lower- and middle-income Ohioans.

Income-tax cuts

The Kasich administration tax plan has a number of elements. The proposal would cut income-tax rates by 23 percent over two years, which comes on top of previous cuts that have slashed the top rate from 7.5 percent in 2004 to 5.33 percent today. Those cuts and other tax changes since then have already provided $20,000 each year on average to filers in the top 1 percent.[2] The rate cut, adjusted to include other changes in the package, is expected to cost $4.6 billion over the two-year budget. Under the proposal, owners of businesses with $2 million or less in annual receipts who pay individual income tax on income from them would see such taxes eliminated (this would add to an existing tax break for business owners). The Kasich administration estimates this would cost nearly $700 million over two years. The proposal also would boost income-tax personal exemptions for those with less than $80,000 in annual income.

Among a host of measures to help pay for the income-tax cuts, the governor proposed means-testing three significant income-tax provisions for seniors: A deduction for Social Security income, a $50 senior credit and a credit for retirement income.[3] Only those with income below $100,000 would continue to be eligible for these deductions or credits. Both these proposals and the increases in personal exemptions would make the income tax more fair, but the proposed rate cuts and business-income tax cuts overwhelm their positive impact.

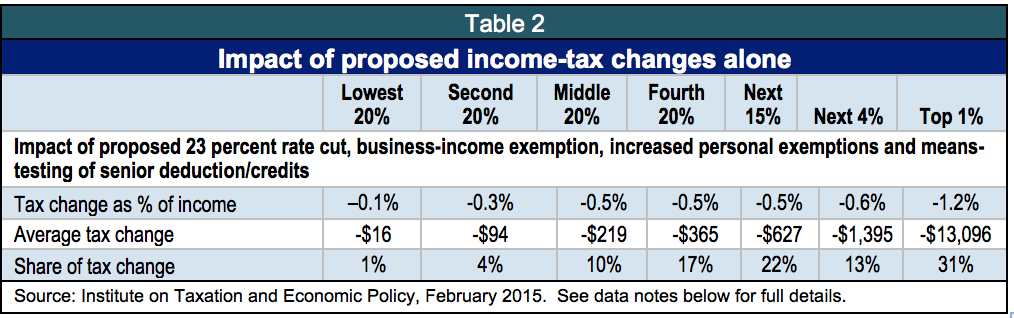

Altogether, ITEP found that the income-tax changes alone would produce a $13,000 gain on average for those in the top 1 percent, who would receive 31 percent of the total tax cut. Those in the middle fifth of the income spectrum would see a reduction of $219 on average, while those in the bottom fifth would receive just $16. Altogether, the bottom 60 percent of Ohioans by income would receive just 15 percent of the income-tax reductions. All this is looking only at the income-tax cuts, not the rest of the tax proposal.

Table 2 shows the total of the proposed income-tax changes:

These income-tax cuts would further tilt Ohio’s state and local tax system in favor of the state’s wealthiest residents. A separate report issued in January 2015 by ITEP showed that overall, nonelderly Ohioans in the top 1 percent pay considerably less of their income in state and local taxes than middle-class and poor Ohioans do (see http://www.policymattersohio.org/tax-report-jan2015).

Sales and other tax changes

ITEP also examined the effects of the administration’s proposals to raise other taxes. These include increasing the state sales-tax rate from 5.75 percent to 6.25 percent, extending the sales tax to a number of additional services and increasing cigarette and other tobacco taxes. The proposal also would raise the rate of the Commercial Activity Tax, while lowering the minimum CAT tax paid by some companies; increase the severance tax on oil and gas produced using high-volume horizontal wells; and reduce or scrap some other tax breaks.

The biggest single increase – more than $1.5 billion over the two-year budget – would come from the rise in the sales-tax rate (the figure doesn’t count Kasich’s proposed expansion of services subject to sales tax). Sales-tax rate increases fall more heavily on low- and middle-income residents, in part, because they spend more of their income than upper-income taxpayers do. The Commercial Activity Tax, which businesses pay on Ohio receipts, ultimately falls on individual taxpayers much like a sales tax.

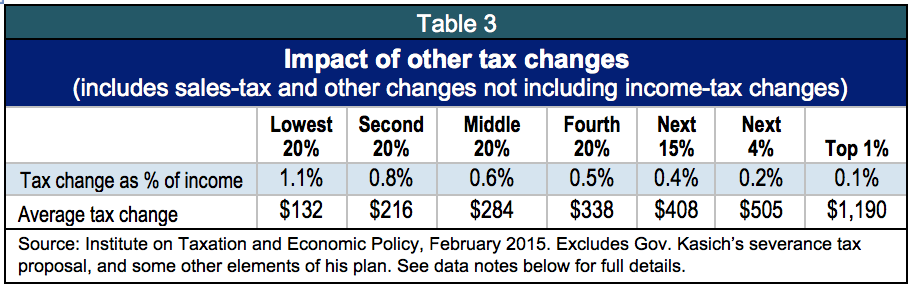

As shown in Table 3, Ohio residents in every income group pay more under the proposed increases in other taxes. The top 1 percent on average would pay $1,190 more a year, while middle-income Ohioans would pay $284 and low-income residents, $132. While the amounts are smaller, for low- and middle-income residents, these increases constitute a larger share of their income.

To offset that, one obvious step is to implement a refundable state Earned Income Tax Credit (EITC), as more than 20 states already have. Ohio has a state EITC, but it is not refundable, meaning it only wipes out state income tax liability and doesn’t help those who earn too little to pay income tax. It also is capped for those earning over $20,000. This tax credit for working families should be refundable like the federal EITC, extending help to far more working Ohioans.[4] The General Assembly also should consider adding sales tax credits, which provide a flat amount for each member of a family below an income threshold.

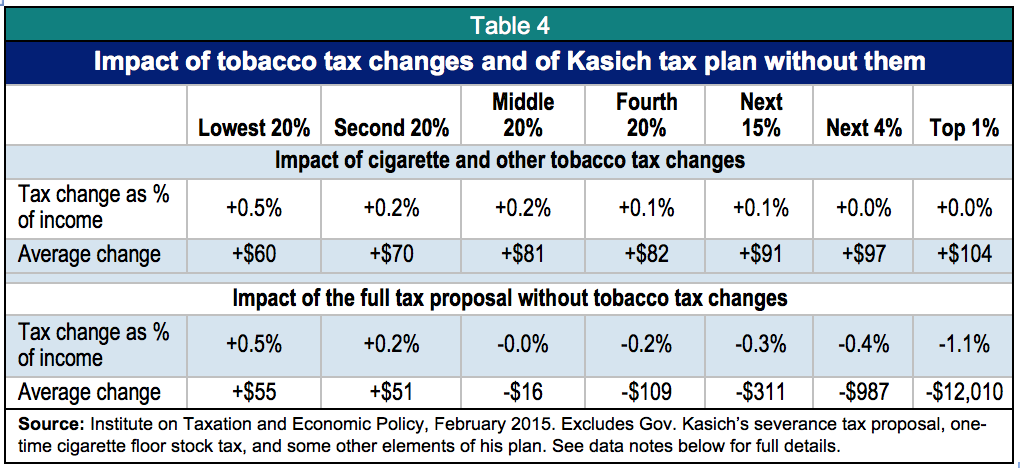

Gov. Kasich’s proposal includes a $1-a-pack increase in the cigarette tax and a boost in the tax on other tobacco taxes. As Table 4 shows, these tobacco-tax changes fall most heavily on the lowest-income Ohioans. Cigarette taxes are charged per unit, not based on price, and lower-income individuals are more likely to smoke.[5]

Of course, only tobacco users will pay the added tobacco taxes. However, as also shown in Table 4, excluding the tobacco tax changes, the proposal remains highly rewarding to Ohio’s most affluent, while costing more on average for the bottom two-fifths of Ohio residents. Middle-income Ohioans see an average annual tax cut of just $16, so little that as a share of income it rounds to zero.

Some of the Kasich administration’s tax proposals, such as the boost in the cigarette tax and the severance tax, serve other worthwhile public policy goals. A higher cigarette tax can reduce smoking and improve public health, while a stronger severance tax can help communities affected by fracking, ensure that Ohio is receiving adequate compensation for the depletion of one-time resources and make our taxes more comparable to those in other states. Broadening the sales tax base can be helpful because our economy has shifted to services, many of which have been untaxed, while the Commercial Activity Tax could well be increased, since it has never come close to replacing the revenue that was lost when it was created in place of two other major business taxes. Policy Matters Ohio previously has endorsed certain other measures in Gov. Kasich’s proposal, such as applying the sales tax to lobbying and debt collection, and reducing the vendor discount for big retailers.[6]

However, these measures and others to modernize Ohio’s tax system should be considered on their own, not to pay for unneeded income-tax rate cuts and business-income tax exemption. We should maintain and bolster the state’s progressive income tax, instead of weakening it as the Kasich administration would do. That would both allow us to invest in needed public services and rebalance the tax system in favor of most Ohioans.

In June 2005, the Ohio General Assembly approved a 21 percent phased-in reduction of income-tax rates; the cuts were increased further in 2013. Since June 2005, Ohio has lost 1.6 percent of its jobs, while the nation as a whole has grown by 4.8 percent. Gov. Kasich’s budget proposal is based on economic forecasts that Ohio will continue to underperform the nation during the upcoming two-year budget period in output, personal income and job growth.[7] There is no reason to believe that another round of tax cuts will bring a different outcome.

Policy Matters Ohio is a nonprofit, nonpartisan state policy research institute with offices in Cleveland and Columbus. The Institute on Taxation and Economic Policy (ITEP) is a non-profit, non-partisan research organization based in Washington, D.C. that works on federal, state, and local tax policy issues. ITEP’s Microsimulation Tax Model allows it to measure the distributional consequences of federal and state tax laws and proposed changes in them, both nationally and on a state-b

[1] ITEP modeled the administration’s full tax proposal except for the severance tax, the one-time cigarette floor stock tax, the elimination of the deduction for early filing and payment of beer and wine tax, the reduction of the watercraft trade-in exemption to 50 percent and the new vapor product tax. See data notes at the end of this report for more description.

[2] Schiller, Zach, "The Great Ohio Tax Shift,” Policy Matters Ohio, Aug. 18, 2014, at http://www.policymattersohio.org/tax-shift-aug2014

[3] This sentence has been corrected from the original version, which said: “Among a host of measures to help pay for the income-tax cuts, the governor proposed means-testing three different income-tax provisions for seniors: A deduction for Social Security income, a $50 senior credit and a credit for lump-sum retirement income.” A similar correction, reflecting that the analysis covers the retirement income credit and not two small lump-sum credits, has also been made below in the Data Notes.

[4] Halbert, Hannah, “Out-of-Step: More Needed to Make Ohio EITC A Credit that Counts,” Policy Matters Ohio, Aug. 26, 2014, at http://www.policymattersohio.org/out-of-step-aug-2014

[5] Centers for Disease Control and Prevention, “Current Cigarette Smoking Among Adults in the United States,” at http://www.cdc.gov/tobacco/data_statistics/fact_sheets/adult_data/cig_smoking/index.htm#national

[6] See Zach Schiller, “Limiting Loopholes: A Dozen Tax Breaks Ohio Could Do Without,” Policy Matters Ohio, November 2008, at http://www.policymattersohio.org/limiting-loopholes-a-dozen-tax-breaks-ohio-can-do-without and Testimony to the House Legislative Study Committee on Ohio’s Tax Structure, Sept. 11, 2011, at http://www.policymattersohio.org/testimony-to-the-house-legislative-study-committee-on-ohio%E2%80%99s-tax-structure

[7] Blueprint for a New Ohio, Governor John R. Kasich’s Fiscal Years 2016-2017 Budget, Section B, Economic Forecast and Income Estimates, p. B-4, at http://blueprint.ohio.gov/doc/budget/State_of_Ohio_Budget_Recommendations_FY-16-17.pdf The forecast, prepared by IHS Global Insight, predicted Ohio’s unemployment rate would be similar to the national rate, though the Office of Budget and Management noted that Ohio’s rate has dropped and may end up below the projection.

Tags

2015Revenue & BudgetTax ExpendituresTax PolicyZach SchillerPhoto Gallery

1 of 22