Healthy Ohio plan is bad medicine

January 12, 2016

Healthy Ohio plan is bad medicine

January 12, 2016

Contact: Wendy Patton, 614.221.4505 or 614.582.0048

Executive summary

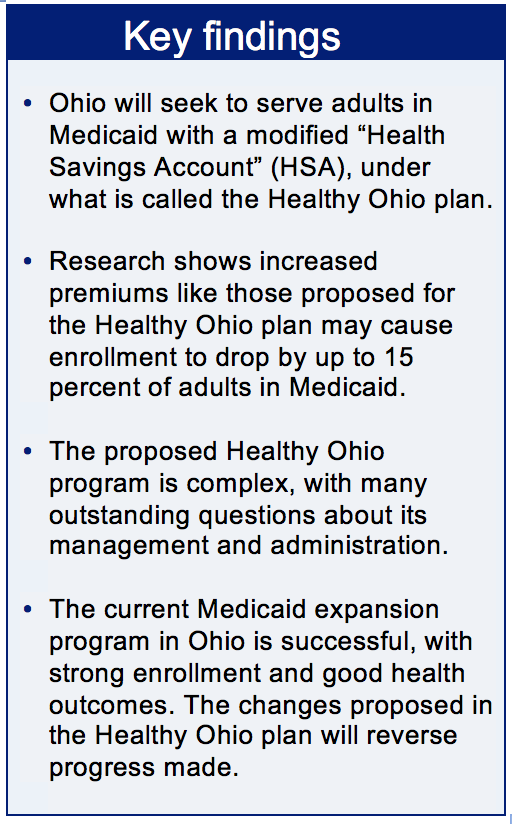

Medicaid expansion has been a success in Ohio, but changes legislators seek would cause many Ohioans to lose their health coverage and lead to higher medical costs.

Medicaid expansion has been a success in Ohio, but changes legislators seek would cause many Ohioans to lose their health coverage and lead to higher medical costs.As part of the 2015 budget bill, Ohio legislators mandated that the Department of Medicaid request a waiver of rules from the federal government in order to change how some of the state’s Medicaid enrollees receive their health insurance. The changes would impose premiums as well as penalties on patients who miss payments. Research shows many would lose health care because of the financial burdens and penalties of the so-called “Healthy Ohio” plan.

Research dating to the 1980s indicates that such plans, by imposing financial barriers for the poor, will work against the kind of good health results Ohio has seen with Medicaid expansion. Ohio’s legislature should repeal the Healthy Ohio plan and stick with its successful Medicaid expansion.

Who is affected by the Healthy Ohio plan?

Around one-third of people in Ohio’s Medicaid program are non-elderly adults without disabilities; this group would be affected. More than half received access to health care through the Medicaid expansion of the Affordable Care Act (“Obamacare”). Almost 650,000 Ohioans have enrolled. About half work, but their wages are so low they live near or in poverty. Health care will be critical to helping them lead better lives: Nearly 70 percent have chronic physical disorders and 42 percent have needed behavioral health treatment.

Is the current Medicaid expansion not working?

Ohio’s Medicaid expansion program is working. Data collected on an early Medicaid expansion pilot program at the MetroHealth Care Plus pilot project in Cleveland finds Ohio’s Medicaid expansion has reduced chronic disease among enrollees with lower-than-expected costs.

But the legislature wants to change it.

How would the Healthy Ohio plan affect health care for low-income people?

While some research finds that imposing premiums and penalties can reduce some costs, it also finds poor health outcomes for people who have low incomes and are in poor health. Poor health outcomes can be expected because of several factors, such as:

- Enrollment will drop. Enrollees in the Healthy Ohio plan will pay a yearly or monthly “premium.” Studies find that among the poorest Medicaid enrollees, boosting costs or charging a premium causes people to drop out. Further, there are penalties – loss of care – with missing payments or paperwork.

- As enrollment drops, care is interrupted. Continuity of care matters in managing common chronic diseases like hypertension and diabetes. Barriers that interrupt consistent, ongoing care result in poor health outcomes.

- Care may be delayed: Current Medicaid coverage is provided for eligible enrollees at the time of application. Under the Healthy Ohio plan, people won’t be enrolled until the first premium is paid. Since people usually enroll when they have a medical problem, this could delay necessary treatment.

Research indicates that the “Healthy Ohio” plan will work against good health outcomes. This is a move in the wrong direction, because the current Medicaid expansion program is very successful. Ohio’s legislature should scrap Healthy Ohio, and the federal government should reject Ohio’s request for a Medicaid waiver. It’s bad medicine for Ohio, and for other states as well.

Introduction

Medicaid expansion has been a success in Ohio, but changes legislators seek would cause many Ohioans to lose their health coverage and lead to higher medical costs.

Medicaid expansion has been a success in Ohio, but changes legislators seek would cause many Ohioans to lose their health coverage and lead to higher medical costs.As part of the 2015 budget bill, Ohio legislators mandated that the Department of Medicaid request a waiver of rules from the federal government in order to change how about a third of the state’s Medicaid enrollees receive their health insurance. The changes would impose premiums, as well as penalties on patients who miss payments. Research shows many would lose health care because of the financial burdens and penalties of the so-called “Healthy Ohio” plan.

Research dating to the 1980s indicates that such plans, by imposing financial barriers for the poor, will work against the good results Ohio has seen with Medicaid expansion. Ohio’s legislature should repeal the mandates to impose the Healthy Ohio plan and stick with its successful Medicaid expansion.

What is Medicaid?

Medicaid provides health care to low-income people, including children, pregnant women, seniors, people with disabilities, and workers who are not offered health coverage by their employer. Medicaid serves about three million Ohioans, a quarter of the population. It covers adults earning less than 138 percent of the federal poverty level (about $16,250 for a single person earning minimum wage). It also assists children in families earning up to 200 percent of poverty ($33,620 for a parent with one child).[1] The federal government pays about two-thirds of Ohio’s Medicaid costs.[2]

The majority of the people served by Medicaid are children, seniors or have disabilities. Around one-third are non-elderly adults without disabilities. About half of this group received access to health care through the Medicaid expansion of the Affordable Care Act (“Obamacare”). Almost 650,000 Ohioans have enrolled under Ohio’s Medicaid expansion.[3] About half work, but their wages are so low they live near or in poverty.[4] Medical care is critical to helping them lead better lives: Nearly 70 percent have chronic physical disorders and 42 percent have needed behavioral health treatment.[5] A pilot program called the MetroHealth Care Plus project in Cleveland clearly showed that Medicaid expansion is improving the health of enrollees (see blue box, below).

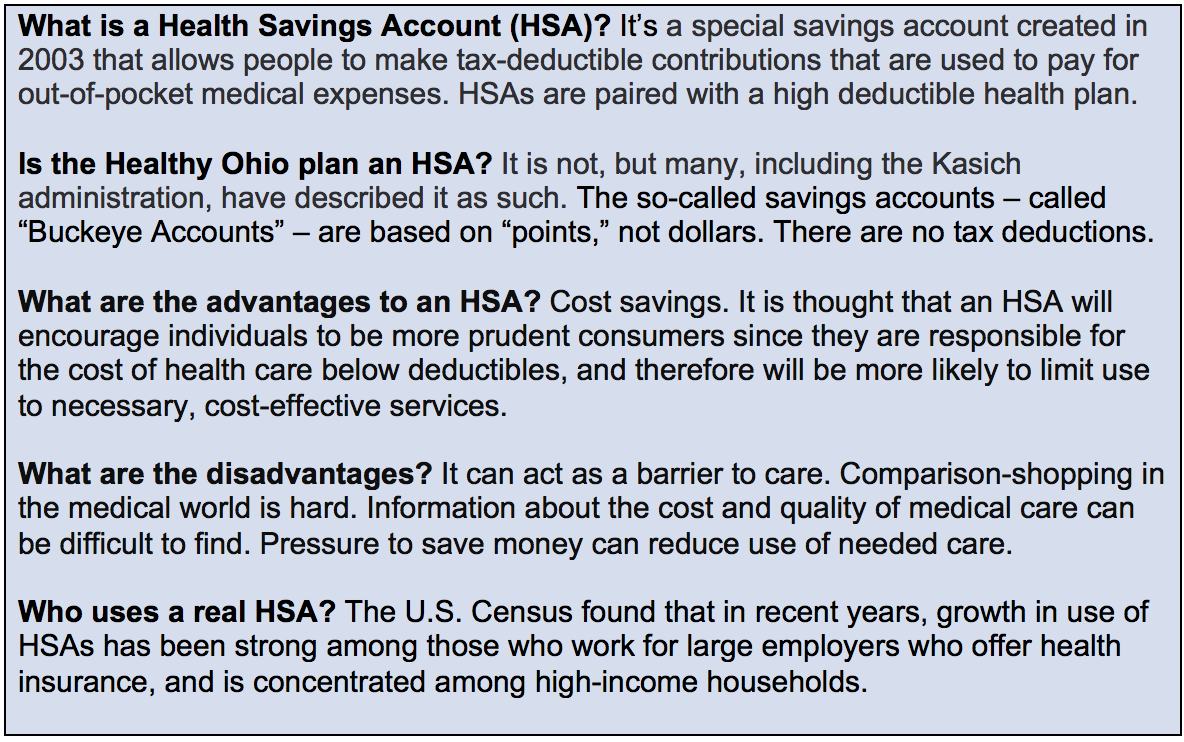

What is the “Healthy Ohio” plan?

The Kasich administration describes the Healthy Ohio plan as a health savings account (HSA) program that would apply to adults in Medicaid.[6]

In fact, the Healthy Ohio plan is not an HSA. An HSA is a special savings account that holds tax-exempt contributions. It is paired with a health insurance plan that has high initial deductibles – in other words, the patient pays for an unusually large share of health care costs out of her own pocket. She makes her payments, however, in tax-exempt dollars from the Health Savings Account.

The Healthy Ohio plan is not based on a savings account, although enrollees would pay a monthly or annual premium (fee) to get into and stay in the program. The account that is set up – called a “Buckeye Account” – is based on “points” not dollars. Medicaid managed care covers significant care costs. Co-pays are covered until the account runs out of funds. Other elements – like penalties, incentives, benchmarks and preferences – are not common elements of private HSAs.

How the Healthy Ohio plan changes Medicaid:

Co-pays and premiums: Medicaid enrollees currently share in the cost of some health services through “co-pays” incurred as services are used. In Ohio, co-pays may be levied on non-emergency services obtained in a hospital or emergency room, dental services, eye examinations, eyeglasses, most brand-name medications and medications that require prior authorization. Co-payments generally range from one to three dollars. Many groups are exempted. Some managed care plans do not charge co-payments.[7]

Co-pays and premiums: Medicaid enrollees currently share in the cost of some health services through “co-pays” incurred as services are used. In Ohio, co-pays may be levied on non-emergency services obtained in a hospital or emergency room, dental services, eye examinations, eyeglasses, most brand-name medications and medications that require prior authorization. Co-payments generally range from one to three dollars. Many groups are exempted. Some managed care plans do not charge co-payments.[7]

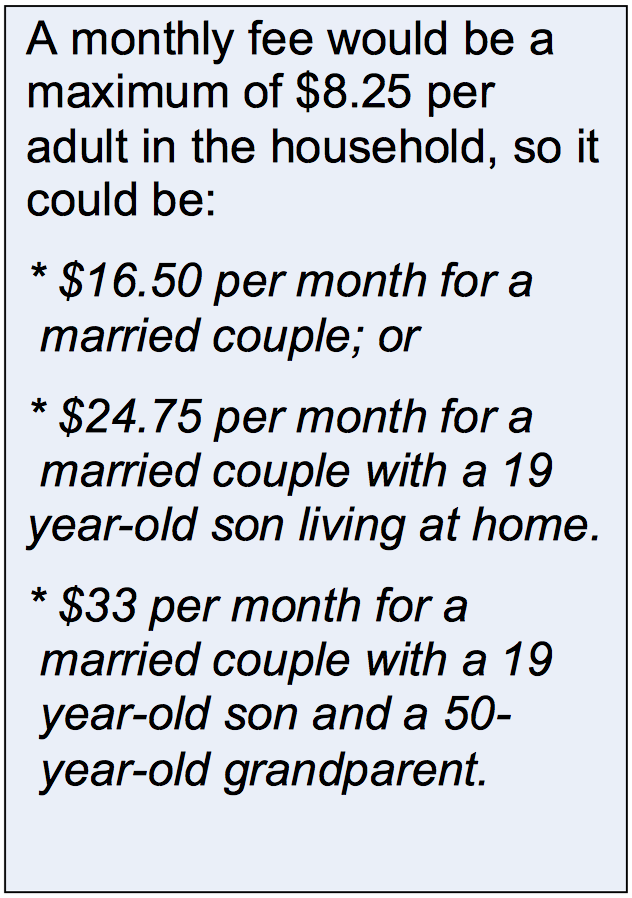

Enrollees in the Healthy Ohio plan will pay a yearly or monthly premium to cover the cost of some of the co-pays. The premium will be the lesser of $99 per year or 2 percent of income. An employer, church or non-profit may contribute, but the individual must pay a minimum of 25 percent of the cost out of his or her own pocket.

Care starts with payment: Medicaid provides eligible enrollees coverage from the date of initial application. This is done to ensure timely and necessary treatment, since people typically enroll when a medical service is needed. The Healthy Ohio plan will not serve people in this fashion. The state Medicaid program will not provide health coverage until the first premium paid.

Special treatment of the medically frail: The language in the budget bill (House Bill 64) does not provide special treatment options for the medically frail, something traditional Medicaid programs and other waiver programs do take into account.

Penalties: People who miss two premium payments will be locked out of the program until they pay what they owe and re-enroll.

Caps: The Healthy Ohio plan caps health care services at $300,000 per year or $1.4 million for a lifetime. Coverage is not lost, but will change within the Medicaid program. People whose care goes beyond the cap will be moved from their managed care provider into the Medicaid “fee for service” program. The language does not include description of how this change will work or provisions for assuring continuity of care.

Points, statements and swipe cards: Enrollee premiums and an annual contribution of $1,000 from Medicaid will fund the Healthy Ohio accounts – called “Buckeye Accounts.” The program will work on “points,” not dollars (although one “point” equals one dollar). Extra points will be awarded through incentives or because of preferred payment methodology (electronic funds transfer). When points are exhausted, the enrollee’s managed care organizations will simply provide coverage. Enrollees will get a monthly statement tallying inventory of points and use of points.

Incentives: Each participant would receive an electronic benefits swipe care, loaded with “points,” which represent the amount of care available to that participant. Enrollees who meet health-care goals or achieve physician-set benchmarks will get extra points.

Preferences: Enrollees with bank accounts who arrange electronic funds transfer for premium payments will get extra points.

Referral to workforce training and placement: Enrollees who are unemployed or working less than 20 hours per week will be referred to the county job training and employment services.

Services: Medicaid services currently provided in Ohio include X-rays, chiropractic, transportation, dental care, vision care and a number of services not included in the language of House Bill 64. The list of services included in the Healthy Ohio plan is more limited:

- Physician,

- Hospital inpatient,

- Hospital outpatient,

- Pregnancy-related,

- Mental health,

- Pharmaceutical,

- Laboratory, and

- Other services the Medicaid director determines necessary.

Research dating back to the 1980s indicates the Healthy Ohio plan, with a modified HSA program design at the core, will not work well for low-income Medicaid enrollees. The reason is simple: Boosting health-care costs through premiums causes people to drop out of Medicaid and not see a doctor when they need care.

Among the low-income in poor health, increased costs leads to poor health outcomes: The RAND Corporation’s Health Insurance Experiment, published in 1982, remains the only long-term, experimental study of cost sharing and its effect on service use, quality of care, and health.[8] This study found higher costs of co-insurance or premiums actually resulted in poor health among the poorest (and sickest) sample members, unlike other segments of the population.[9]

Among the low-income in poor health, increased costs leads to poor health outcomes: The RAND Corporation’s Health Insurance Experiment, published in 1982, remains the only long-term, experimental study of cost sharing and its effect on service use, quality of care, and health.[8] This study found higher costs of co-insurance or premiums actually resulted in poor health among the poorest (and sickest) sample members, unlike other segments of the population.[9]

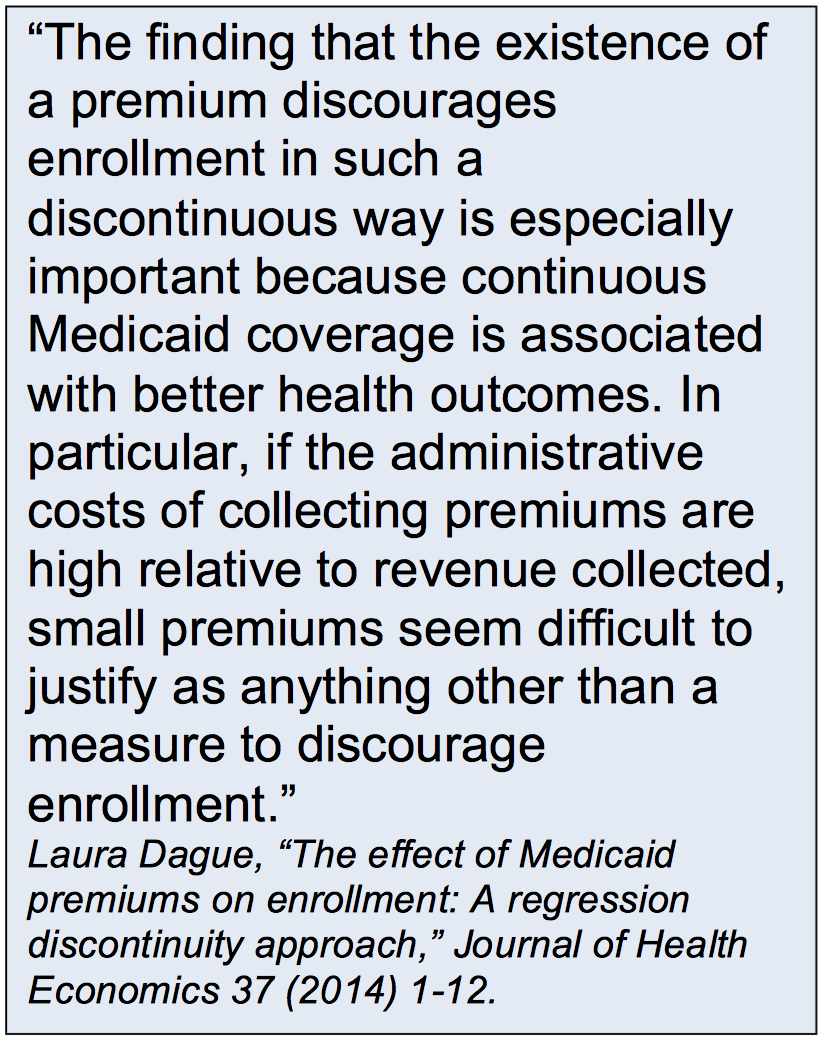

Premiums of any level cause low-income enrollees to drop out: A recent study in the Journal of Health Economics (Dague, 2014) found that among the poorest Medicaid enrollees – those earning less than 150 percent of the federal poverty level – a monthly premium of up to $10 results in fewer months of continuous enrollment for both adults and children. These effects are concentrated in the first few months of coverage: enrollees are 12 to15 percent more likely to leave the program within 12 months.[10]

Continuity of care matters in managing common chronic diseases.[11] Poverty interacts with chronic diseases like diabetes, hypertension and depression.[12] Lack of access to nutritious food and health care compound health problems.[13] Barriers that interrupt consistent, ongoing care result in poor health outcomes.

The U.S. Department of Health and Human Services published research findings in July 2015 that found increased costs make it harder for poor families to access needed health care and maintain coverage. Key findings include:[14]

- Low-income individuals are especially sensitive to increases in medical out-of-pocket costs. Modest co-payments can have the effect of reducing access to necessary medical care.

- Medical fees, premiums, and co-payments could contribute to the financial burden on poor adults who need to visit medical providers.

- The problem is even more pronounced for families living in the deepest levels of poverty, who effectively have no money available to cover out-of-pocket medical expenses, including co-pays for medical visits.

People without bank accounts face special barriers: Many low-income families lack bank accounts, making timely payments expensive and logistically challenging. A Federal Deposit Insurance Corporation 2013 survey found that over 328,000 Ohio households – 7.2 percent – have no bank account.[15] These households cannot pay bills online or with credit cards. Purchasing a money order adds to the overall cost of the premium.

Interrupted care leads to poor health outcomes: Some months, enrollees may not have enough income to make a payment. Coverage may be lost. If the enrollee has a chronic disease such as diabetes or hypertension, lack of treatment could cause serious medical complications and be costly to the health-care system.

Assignment and tracking of points may be administratively expensive. Tracking premiums and co-pays have proven expensive in other states.[16] The Ohio Hospital Association, in its first issue brief about the proposed plan, expresses concerns about administrative costs (see blue box, below).

Incentives and benchmarks could discriminate against the poorest: Extra points are to be given for yet-to-be defined “healthy behaviors” and for meeting physician-set benchmarks. This could discriminate against those who lack access to health basics: Transit to get to stores with healthy food, for example, or whose neighborhoods are too unsafe to permit healthy exercise. Extra points are also to be given to those who arrange to pay their premiums through electronic funds transfer. This discriminates against those who have no Internet access and those too poor to have a bank account. Ohio has a large number of people without bank accounts,[17] many of whom are likely to be in need of Medicaid.

Why Ohio wants changes that conflict with Medicaid goals

Research finds savings associated with health savings accounts, but also finds dangers of curtailed care for people of poor health and low income.[18] Medicaid is supposed to improve the health of low-income people. The HSA program design has inherent conflicts with Medicaid program goals. Reasons for embrace of the HSA model, and dangers of that model, are explored below. The question is whether savings outweigh the likely cost in terms of health outcomes – particularly when Ohio’s current Medicaid expansion program demonstrates successful outcomes in both cost savings and improved health.

To cut costs through market forces: The Heritage Foundation has strongly promoted the use of tax credits and health savings accounts as an alternative to the Affordable Care Act. Their research was cited in testimony to the House Healthcare Committee’s Summer Study Committee, which suggested a health savings account-type program design would reduce health-care costs to the state as consumers shop around for services based on cost and impose competitive market forces on health care services.[19]

To reduce enrollment: Premiums imposed on low-income Medicaid enrollees raise far too little money to help pay for care in any meaningful way[20] and studies find increased costs and/or premiums of any level cause low-income people to drop out of health-care enrollment. Researchers writing for the New England Journal of Medicine concluded: “…. premiums may save states money, but primarily by keeping people uninsured, thereby working against the ACA's primary goal of expanding insurance coverage.” [21]

To curtail ‘over-use’ of health care by low-income individuals. Some assume low-income people over-utilize health services. Medicaid program design based on modified HSAs are proposed to reduce their use of services.[22] However, research shows that poor people in America underutilize health services compared to other developed nations.[23]

To familiarize Medicaid enrollees with the private health insurance market: States experimenting with the HSA model say this will teach people how to use private health insurance. Ohio’s Medicaid program is operated by managed care organizations (MCO), which treat Medicaid and marketplace customers in the same way: The Medicaid enrollee is familiar with the private health system through their MCO. Perhaps of greater importance is that the Medicaid program is not just a way to cover a large group of people, it is the public health-care program specifically designed to meet the needs of low-income individuals.[24]

To encourage use of preventive care to reduce health care costs: Some states have implemented the use of incentives to encourage use of preventive care and decrease the need for future high-cost treatments and hospital use. The effectiveness of such incentives has been questioned in many reviews, based on high costs of infrastructure start-up, marketing and administration.[25] Evaluation of some programs – like that of West Virginia and Wisconsin – have identified specific problems that prevented attainment of health outcome goals or reduced care for some beneficiaries.[26]

The RAND corporation, reviewing studies on the effect of high deductible health plans coupled with HSAs, concluded: “While evidence suggests that the health of the overall population may not change with increased cost sharing, the health of individuals with low income and greater health care needs may decline.”[27]

To promote “Personal responsibility”: Some blame the sick or unhealthy individual for bad personal choices. Those promoting “personal responsibility” in health care encourage the use of incentives and penalties in Medicaid to get people to make “right” choices instead of “wrong” choices. In health care, however, personal responsibility is exhibited when people enroll in Medicaid, see a doctor regularly and take control of chronic disease management. Ohio’s current Medicaid expansion has had resounding success in part because it gives people the tools they need to follow through on the behaviors that will improve health.

The Healthy Ohio plan will refer enrollees without a job or who work less than 20 hours per week to county employment services. Nine of Ohio’s 12 largest occupational groups pay so little at the median wage that a parent with two children would be eligible for Medicaid.[28] Lack of jobs that pay a living wage is a formidable barrier to self-sufficiency throughout Ohio.

Have other states implemented strategies like this?

The Affordable Care Act initially required states to expand Medicaid, but the Supreme Court ruled that the states could decide. Several states asked the federal government to allow them to change rules about the program for this population.[29] Such new program designs are referred to as “waivers” of Section 1115 of the Social Security Act, which is the section authorizing the Medicaid program. Section 1115 waiver programs are considered “demonstration” projects. They are intended to test approaches that would allow the Medicaid program to work better.

Some of the waivers for the Medicaid expansion population have imposed premiums, created incentives or penalties, or in some cases, curtailed services. The federal government approved these waivers to encourage Medicaid expansion. What is different about the Healthy Ohio waiver is that Ohio has already expanded Medicaid. Ohio’s plan is successful. An average of almost 650,000 people are expected to get coverage under the Medicaid expansion in state fiscal year 2016.[30] Health outcomes – especially in terms of improving chronic disease – have been good and per-participant costs, lower than expected.[31] Hospitals have seen strengthened bottom lines.[32] The state reports health care utilization by this population declined over the course of the first year of enrollment.[33] Ohio does not need to experiment with new approaches to improve its Medicaid expansion.

There are other reasons the federal government should not approve a waiver request like that of the Healthy Ohio plan. Many elements of the proposal would replicate other demonstration programs that have yet to be evaluated. Until federal evaluations provide definitive proof that premiums, penalties, incentives and other features of the Healthy Ohio plan improve health outcomes for low-income people, no more waivers like this should be approved – particularly in light of research that indicates some elements will likely cause poor health outcomes.

Summary and conclusion

Ohio has a successful Medicaid expansion program. Enrollment has exceeded projections, indicating successful marketing and outreach. Health outcomes are impressive. The program has also yielded cost savings.

The budget bill for 2016-17 mandated changes for Medicaid expansion. It created the Healthy Ohio plan, which would levy yearly or monthly premiums on the poorest Ohioans and impose penalties (loss of care) on those who cannot pay. Provisions meant to encourage “healthy behaviors” could discriminate against people whose neighborhoods lack grocery stores with nutritious food or outdoor areas in which to exercise safely. The plan also discriminates against those without bank accounts, because the plan offers greater access to care to those who can arrange electronic funds transfers to pay monthly or annual premiums. While some point to potential cost savings from an HSA type of plan, this program design does not create true HSAs – a tool for high-income employees of large firms paired with high-deductible insurance plans – for Medicaid enrollees.

Research indicates a move to the Healthy Ohio plan will work against the kind of good health outcomes Ohio has seen with Medicaid expansion. Ohio’s legislature should repeal the mandates to impose the Healthy Ohio plan and stick with its successful Medicaid expansion. The federal government should reject Ohio’s request for a Medicaid waiver. It is bad medicine for Ohio, and for other states as well.

APPENDIX: Studies show: costs pose barriers to health care for the poor

Improving health and controlling costs under national health-care reform depends on expanded preventive care and predictable payment for providers. Requiring a financial contribution discourages low-income people from seeking health care and, in some cases, leads to an increase in expensive emergency room treatment that goes unpaid, a substantial body of research finds.[34]

The RAND Health Insurance Experiment of the 1970s, a definitive study on this issue, found that co-payments led to a much larger reduction in use of medical care by low-income adults and children than by those with higher incomes. Low-income families lost far more because of financial contribution requirements than middle and high-income people. [35]

State-level studies assessing how financial requirements affect the use of health care by low-income people over the past decade corroborate these findings.

- Laura Dague, writing for the Journal Of Health Economics, cited studies on outcomes of interrupted (discontinuous) health care (L. Dague / Journal of Health Economics 37 (2014) 1–12). She points out that: “Length of continuous enrollment in Medicaid is important because even though Medicaid coverage is sometimes thought of as implicit, numerous studies have shown that continuous Medicaid coverage is associated with better health outcomes.

- Bindman et al. (2008)[36] show ambulatory care-sensitive hospitalizations are more likely among those with discontinuous Medicaid spells, and

- Hall et al. (2008) show diabetics with continuous Medicaid coverage have lower health care costs than those with discontinuous coverage.[37]

- While it is possible those who leave Medicaid switch to employer-sponsored insurance or the individual market (rather than to being uninsured), Lavarreda et al. (2008) find those who switch insurance types are less likely to report a usual source of care.[38]

- The Oregon Health Insurance Experiment team has shown that Medicaid increases use of preventive care, self-reported health, mental health, and financial well-being, although two-year clinical outcomes were mixed (Finkelstein et al., 2012;[39] Baicker et al., 2013a[40]).

- DeLeire et al., 2013 show that for a relatively sick population, Medicaid can decrease hospitalization rates.[41]

- Wisconsin imposed premiums of 3 percent of household income on adult Medicaid patients in July 2012. Three months later, nearly a quarter of this group had been dropped from Medicaid because of non-payment.[42]

- Physicians at Minneapolis’ main public hospital surveyed patients attending medical clinics in mid-2004. Of 62 patients covered by Medicaid or medical assistance, more than half (32) reported that they had been unable to get their prescriptions at least once in the last six months because of co-payments of $3 for brand name drugs or $1 for generic drugs. Eleven of the patients who failed to get their medications had 27 subsequent emergency room visits and hospital admissions for related disorders. For example, patients with high blood pressure, diabetes or asthma who could not get their medications experienced strokes, asthma attacks and complications due to diabetes. [43]

- More than a decade ago, Oregon raised premiums for adults with incomes below the poverty line. Premiums ranged from $6 per month for people with no income to $20 per month for people with incomes at the poverty line. Nine months later, nearly half had lost their coverage. About three-quarters of them became uninsured.”[44]

- A 2003 survey of low-income adults covered by Medicaid in Utah found 27 percent had lost coverage and more than a quarter of them cited co-pays as the cause. Of those who did not re-enroll, 20 percent reported co-pays were too high to use services. About half of all respondents who had left Medicaid had not seen a physician for 12 months. Many who needed care reported difficulty getting services, particularly mental health care, alcohol/drug treatment, and dental services.[45]

- In January 2004, Vermont increased premiums in its Medicaid and State Children’s Health Insurance programs. During the first month of increased premiums, enrollment declined by 11 percent, or 4,500 people. Cost was cited as the reason by 70 percent of those who lost Vermont’s coverage, which included adults with incomes between 50 and 185 percent of poverty. [46]

- In January 2002, Rhode Island began charging premiums ranging from $43-$58 per month to families with incomes above 150 percent of poverty. Nearly one in five families could not afford to pay and dropped coverage over the next three months. Nearly half of surveyed families who lost coverage reported being unable to afford the premium as the reason.

- In Maryland, families were subject to $37-per-month premiums in the children’s insurance program. Coverage was dropped for 28 percent of children. Parents cited a premium-related reason in nearly one of five cases, and state legislators subsequently eliminated the premiums.

[2] The federal share is higher for some populations. For example, the federal government pays 100 percent of the Medicaid expansion population health care costs.

[3] Ohio Department of Medicaid, Medicaid caseload report for November 2015 at http://medicaid.ohio.gov/Portals/0/Resources/Reports/Caseload/2015/11-Caseload.pdf. Accessed 12/31/2015.

[4] Testimony of Director John McCarthy of the Ohio Department of Medicaid to the Senate Medicaid Committee on 2016-17 budget priorities (May 5, 2015) indicates that 43 percent of Medicaid expansion enrollees report earned income. Another 50 percent were registered through the MetroHealth pilot project and earnings are not tracked.

[5] Testimony of Director John McCarthy of the Ohio Department of Medicaid to the Senate Medicaid Committee on 2016-17 budget priorities (May 5, 2015).

[6] “Health Savings Accounts”, Ohio’s Governor’s Office of Health Transformation at http://www.healthtransformation.ohio.gov/LinkClick.aspx?fileticket=RSPpS3DA4pc%3D&tabid=136

[7] “Medicaid Basics 2015,” Health Policy Institute of Ohio at file:///Users/wendypatton/Documents/Medicaid%202015/MedicaidBasics_2015_Final.pdf

[8] Brook, Robert H., Emmett B. Keeler, Kathleen N. Lohr, Joseph P. Newhouse, John E. Ware, William H. Rogers, Allyson Ross Davies, Cathy D. Sherbourne, George A. Goldberg, Patricia Camp, Caren Kamberg, Arleen Leibowitz, Joan Keesey and David Reboussin. “The Health Insurance Experiment: A Classic RAND Study Speaks to the Current Health Care Reform Debate.” Santa Monica, CA: RAND Corporation, 2006. http://www.rand.org/pubs/research_briefs/RB9174.html.

[9] Newhouse, 1993, cited in Laura Dague, “The effect of Medicaid premiums on enrollment: A regression discontinuity approach,” Journal of Health Economics 37 (2014) 1-12. http://www.rand.org/pubs/research_briefs/RB9174.html

[10] Dague, Op.Cit.

[11] “The Role of Medicaid for adults with chronic illnesses,” Kaiser Family Foundation, November, 2102 at https://kaiserfamilyfoundation.files.wordpress.com/2013/01/8383.pdf

[12] The World Health Organization, “Chronic Disease and Health Promotion, Chapter two – Chronic Diseases and Poverty” at http://www.who.int/chp/chronic_disease_report/part2_ch2/en/

[13] Danielle Kurtzlaben, “Americans in poverty at greater risk for chronic diseases,” U.S. News and World Report, October 30, 2012 at http://www.usnews.com/news/articles/2012/10/30/americans-in-poverty-at-greater-risk-for-chronic-health-problems

[14] Office of the Assistant Secretary for Planning and Evaluation, “Financial Condition and Health Care Burdens of People in Deep Poverty,” United States Department of Health and Human Services, July 16, 2015 at

[15] Federal Deposit Insurance Corporation, 2013 FDIC National Survey of Unbanked and Underbanked Households (Appendices), Table G-2, page 118, https://www.fdic.gov/householdsurvey/2013appendix.pdf

[16] Virginia Department of Medical Assistance Services memo, 5/15/2002. See also, L. Summer & C. Mann, “Instability of Public Health Insurance Coverage for Children and Their Families: Causes, Consequences, and Remedies,” The Commonwealth Fund (June 2006). Cited in Tricia Brooks, Handle with Care: How Premiums Are Administered in Medicaid, CHIP and the Marketplace Matters, Georgetown University Center for Families and Children at http://www.healthreformgps.org/wp-content/uploads/Handle-with-Care-How-Premiums-Are-Administered.pdf

[17] Cleveland ranked 4th among the top ten most unbanked big cities in the nation; Cleveland and Cincinnati both made the top 10 list in terms of cities with the largest numbers of census tracts with high proportion of unbanked households. Corporation for Enterprise Development at http://cfed.org/assets/pdfs/Most_Unbanked_Places_in_America.pdf.

[18] Karen Davis, Michelle M. Doty and Alice Ho, “How high is too high? The implications of high deductible health plans”, the Commonwealth Fund, 2005 at http://www.commonwealthfund.org/~/media/files/publications/fund-report/2005/apr/how-high-is-too-high--implications-of-high-deductible-health-plans/816_davis_how_high_is_too_high_impl_hdhps-pdf.pdf

[19] Greg Lawson, “Interested party testimony submitted to the House Healthcare Efficiencies Summer Study Committee, September 16, 2015 at http://www.buckeyeinstitute.org/uploads/files/150915%20HouseHealthcareEfficienciesComm%20(Final)(1).pdf

[19] http://www.mayoclinic.org/healthy-lifestyle/consumer-health/in-depth/health-savings-accounts/art-20044058

[20] For example, the Kasich Administration initially estimated the premiums proposed in the executive budget -- twice the level of the “Healthy Ohio” plan -- would only generate up to $3.2 million dollars by 2017, a tiny sum in a multi-billion dollar program. See Ohio Legislative Service Commission, Greenbook for Ohio Department of Medicaid, House Bill 64 of the 131st General Assembly.

[21] Brendan Saloner, Ph.D., Lindsay Sabik, Ph.D., and Benjamin D. Sommers, M.D., Ph.D., Op. Cit.

[22] “Medicaid bill loses savings accounts”, Wyoming Tribune Eagle (Wyoming.com) at http://www.wyomingnews.com/articles/2015/01/31/news/19local_01-31-15.txt#.VoPpxBHoUlY “New Medicaid Expansion Plan Emerges in the Senate,” WYPOLS at http://wypols.com/2015/01/27/new-medicaid-expansion-bill-emerges-senate/

[23] Americans are much more likely than their counterparts in other countries to say they did not visit a physician, fill a prescription, or get a recommended test, treatment, or follow-up care because of costs. In a comparison among developed nations, disparities in care between people in above-average and below-average income groups were greatest in the United States Karen Davis, Cathy Schoen, Stephen C. Schoenbaum, Anne-Marie Audet, Michelle Doty, and Katie Tenney, Mirror Mirror on the Wall: The Quality of American Health Care Through the Patients’ Lens, The Commonwealth Fund, forthcoming October 2003.

[24] Leo Cuello, “What Makes Medicaid, Medicaid: Five Reasons Why Medicaid Is Essential to Low-Income People,” January 14, 2015, http://www.healthlaw.org/issues/medicaid/waivers/what-makes-medicaid-medicaid-five-reasons-why-medicaid-is-essential-to-low-income-people#.VmBOetIrLGg

[25] Kaiser Family Foundation issues brief (https://kaiserfamilyfoundation.files.wordpress.com/2014/09/8631-an-overview-of-medicaid-incentives-for-the-prevention-of-chronic-diseases-mipcd-grants.pdf); see also Judith Solomon, West Virginia’s Medicaid Changes Unlikely to Reduce State Costs or Improve Beneficiaries’ Health (Washington, DC: Center on Budget and Policy Priorities, May 2006), http://www.cbpp.org/cms/?fa=view&id=336; Families USA, Mountain Health Choices: An Unhealthy Choice for West Virginians (Washington, DC: Families USA, August 2008).

[26] http://ccf.georgetown.edu/wp-content/uploads/2012/03/WV-factsheet-2008.pdf; see also Wisconsin Department of Health Services. “Do Incentives Work for Medicaid Members? A Study of Six Pilot Projects.” May 2013. Available at: http://www.dhs.wisconsin.gov/publications/p0/p00499.pdf.

[27] “Analysis of High Deductible Health Plans,” RAND corporation at http://www.rand.org/pubs/technical_reports/TR562z4/analysis-of-high-deductible-health-plans.html#health

[28] Median wages of three-quarters of the dozen largest occupational groups listed in the Ohio Labor Market’s “Employment and Wages” database would leave a parent with two children eligible for Medicaid. See Occupational Wage Estimates at http://ohiolmi.com/asp/oeswage/SOCWage.asp?Source=Wage (Based on the Bureau of Labor Statistics Occupational Employment Statistics)

[29] The Kaiser Family Foundation tracks status of Medicaid expansion programs. Thirty-one states (including District of Columbia) have expanded Medicaid to cover non-elderly adults under the Affordable Care Act (http://kff.org/health-reform/slide/current-status-of-the-medicaid-expansion-decision/); of these, six or 20 percent have requested or are implementing experimental programs under Medicaid waiver provisions (http://kff.org/medicaid/issue-brief/the-aca-and-medicaid-expansion-waivers/).

[30] Ohio Department of Medicaid, Medicaid caseload report for November 2015 at http://medicaid.ohio.gov/Portals/0/Resources/Reports/Caseload/2015/11-Caseload.pdf. Accessed 12/31/2015.

[31] Randall D. Cebul, Thomas E. Love, Douglas Einstadter, Alice S. Petrulis and John R. Corlett, Op.Cit.

[32] Policy Matters Ohio, “Medicaid Expansion Benefits Ohio,” September 2014 at http://www.policymattersohio.org/wp-content/uploads/2014/10/Medicaid.pdf

[33] Testimony of Ohio Department of Medicaid Director John McCarthy to the Senate Committee on Medicaid, May 5, 2015, Op.Cit.

[34]“Premiums and Cost-Sharing in Medicaid: A Review of Research Findings,” Kaiser Commission on Medicaid and the Uninsured, February 2013 at http://kaiserfamilyfoundation.files.wordpress.com/2013/02/8417.pdf ; Samantha Artiga and Molly O’Malley, “Increasing Premiums and Cost Sharing in Medicaid and SCHIP: Recent State Experiences,” Kaiser Commission on Medicaid and the Uninsured at http://kaiserfamilyfoundation.files.wordpress.com/2013/01/increasing-premiums-and-cost-sharing-in-medicaid-and-schip-recent-state-experiences-issue-paper.pdf Leighton Ku and Victoria Wachino, “The Effect of Increased Cost-Sharing in Medicaid.” July 2005 at http://www.cbpp.org/cms/?fa=view&id=321

[35] The RAND study found that co-payments did not significantly harm the health of middle- and upper-income people but did lead to poorer health for those with low incomes. The study found that among low-income adults and children, health status was considerably worse for those who had to make co-payments than for those who did not. (In the RAND study, low income was defined as the lowest third of the income distribution, which is roughly equivalent to being below 200 percent of the poverty line.) For example, co-payments increased the risk of dying by about 10 percent for low-income adults at risk of heart disease - Joseph Newhouse, Free For All? Lessons from the Rand Health Insurance Experiment, Cambridge: Harvard University Press, 1996, cited in Leighton Ku and Victoria Wachino, “The Effect of Increased Cost-Sharing in Medicaid.” July 2005 at http://www.cbpp.org/cms/?fa=view&id=321

[36] Bindman, A.B., Chattopadhyay, A., Auerback, G.M., 2008. Interruptions in Medicaid coverage and risk for hospitalization for ambulatory care–sensitive conditions. Annals of Internal Medicine 149 (12), 854–860.

[37] Hall, A.G., Harman, J.S., Zhang, J.Y., 2008. Lapses in Medicaid coverage impact on cost and utilization among individuals with diabetes enrolled in Medicaid. Medical Care 46 (12), 1219–1225.

[38] Lavarreda, S.A., Garchell, M., Ponce, N., Brown, E.R., Chia, Y.J., 2008. Switching health insurance and its effects on access to physician services. Medical Care 46 (10), 1055–1063.

[39] Finkelstein, A., Baicker, K., Taubman, S., Wright, B., Bernstein, M., Gruber, J., New- house, J.P., Allen, H., the Oregon Health Study Group, 2012. The Oregon health insurance experiment: evidence from the first year. Quarterly Journal of Eco- nomics 127 (3).

[40] Baicker, K., Finkelstein, A., Song, J., Taubman, S., 2013b. The Impact of Medicaid on Labor Force Activity and Program Participation: Evidence from the Oregon Health Insurance Experiment, NBER Working Paper 19547.

[41] DeLeire, T., Dague, L., Leininger, L., Friedsam, D., Voskuil, K., 2013. Wisconsin experience indicates that expanding public insurance to low-income childless adults has health care impacts. Health Affairs 32 (6), 1037–1045.

[42] State of Wisconsin Department of Health Services “Wisconsin Medicaid Premium Reforms: Preliminary Price Impact,” Table 4: Premium enrollment impacts. Findingshttp://www.dhs.wisconsin.gov/publications/P0/P00447.pdf

[43] Melody Mendiola, Kevin Larsen, et al. “Medicaid Patients Perceive Co-pays as a Barrier to Medication Compliance,” Hennepin County Medical Center, Minneapolis, MN, presented at the Society of General Internal Medicine national conference, May 2005 and American College of Physicians Minnesota chapter conference, Nov. 2004.

[44] Center on Budget and Policy Priorities and Georgetown University Center for Children and Families, Letter to Secretary Kathleen Sibelius regarding proposals for the Iowa Marketplace Choice Plan and Iowa Wellness Plan, September 26, 2013 at http://ccf.georgetown.edu/wp-content/uploads/2013/09/IA-Longer-Comments-Final.pdf

[45] Utah Primary Care Network Disenrollment Report. Utah Department of Health Center for Health Data, Office of Health Care Statistics, August 2004, cited in “Premiums and Cost-Sharing in Medicaid: A Review of Research Findings,” Kaiser Commission on Medicaid and the Uninsured, February 2013 at http://kaiserfamilyfoundation.files.wordpress.com/2013/02/8417.pdf

[46] Kaiser Health http://kaiserfamilyfoundation.files.wordpress.com/2013/01/increasing-premiums-and-cost-sharing-in-medicaid-and-schip-recent-state-experiences-issue-paper.pdf

Tags

2016MedicaidRevenue & BudgetWendy PattonPhoto Gallery

1 of 22