Ohio House moves Medicaid in wrong direction

April 23, 2015

Ohio House moves Medicaid in wrong direction

April 23, 2015

Contact: Wendy Patton, 614.221.4505

By Wendy Patton

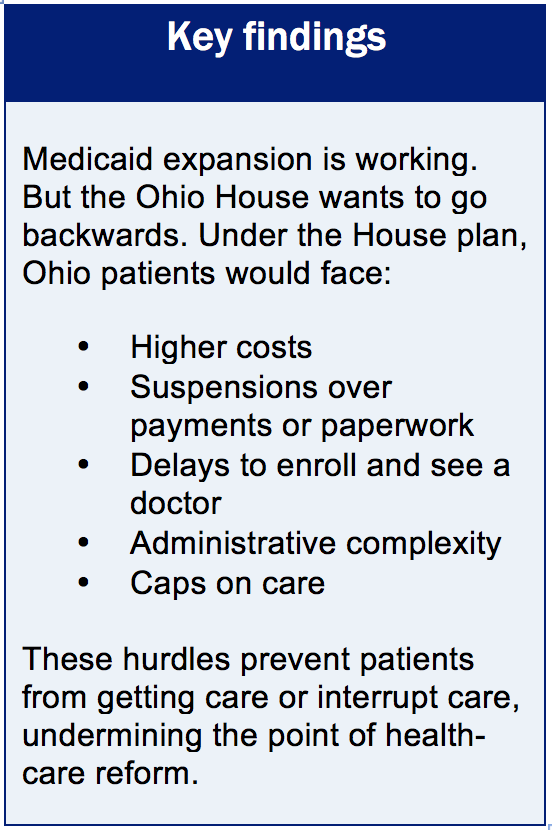

Ohio’s Medicaid expansion has been an unqualified success, with more than half a million Ohioans newly insured and billions of federal dollars pumped into the Ohio economy. Health care providers report better bottom lines and healthier patients.[1] But the Ohio House of Representatives took a giant step backwards in its version of the fiscal year 2016-17 budget with a proposal that would make it more difficult for low-income families and their children to obtain and maintain health coverage. The House plan, outlined in substitute House Bill 64, directs the state to pursue a waiver of Medicaid rules to implement a new program design. This could jeopardize health coverage for hundreds of thousands of adults and children.

Ohio’s Medicaid expansion has been an unqualified success, with more than half a million Ohioans newly insured and billions of federal dollars pumped into the Ohio economy. Health care providers report better bottom lines and healthier patients.[1] But the Ohio House of Representatives took a giant step backwards in its version of the fiscal year 2016-17 budget with a proposal that would make it more difficult for low-income families and their children to obtain and maintain health coverage. The House plan, outlined in substitute House Bill 64, directs the state to pursue a waiver of Medicaid rules to implement a new program design. This could jeopardize health coverage for hundreds of thousands of adults and children.The Affordable Care Act (ACA) included a federally financed plan to expand Medicaid coverage to adults, aged, blind and disabled people, and children. This was done to address a basic human need for health care, to control burgeoning costs of untreated chronic conditions like heart disease and diabetes, and to strengthen a health care system burdened by medical crises. Thirty states, including the District of Columbia, have taken the federal money.

Ohio’s Medicaid expansion gets good reviews in national studies. It allows people to see a doctor and to get needed health care they could not otherwise obtain,[2] with service and quality of care similar to that of private pay care.[3]

Ohio, like most states, expanded Medicaid by expanding the state Medicaid plans to include people who were newly eligible. Some states proceeded differently, asking for a waiver of certain Medicaid rules, which is allowed under Section 1115 of the Social Security Act. The new version of House Bill 64 would abandon Ohio’s successful plan model and require the Director of Medicaid to seek a waiver of many Medicaid rules. The plan, misleadingly named “Healthy Ohio”, would jeopardize the state’s success in extending health coverage to its most vulnerable residents.

Troublesome components of the proposal include:

- Raises costs on the poorest families: Monthly charges would be imposed on even the poorest families, even those with children. Medicaid enrollees would contribute up to 2 percent of family income to an account, identified in the legislation as a “modified health savings account.” Even people and families without income would be required to contribute or risk losing access to health care. A managed care plan or employer would be allowed to contribute but the individual would have to provide at least 25 percent of the contribution.

- Lock-out: A person or family can be suspended or locked out of health coverage if a monthly premium is not paid within 60 days, or if the patient (or their parent, for children) fails to provide redetermination documentation after 60 days. The suspension is for 12 months.

- Favors those with bank accounts: Those who have bank accounts and can arrange electronic transfers get more care “points’’ than others. Ohio is a state with a high proportion of families without bank accounts.[4] They are more likely to be the poorest of families. This is contrary to the core purpose of Medicaid: covering costs of care people cannot afford.

- Wait time: Beneficiaries could be forced to wait days or months for care. Before getting care, patients would need to submit an application , have the account created, make an initial payment, and establish “points”.

- Administrative complexity The Medicaid proposal for adults, families and children will be administratively complex. Ostensibly, making monthly payments would help patients adjust to the private market. However, payments under this plan would be translated into “points,” not dollars, which differ from real-world transactions.

- Annual and lifetime caps on care: Coverage is suspended if the cost of care exceeds the $300,000 annual cap or the $1,000,000 lifetime cap. Annual suspensions last until the next year of coverage. The plan calls for arranging a catastrophic health care plan for those who exceed annual or lifetime caps, but there is no indication of how this would be financed or of the impact on continuity of care for sick patients.

The federal government has certain smart requirements that are part of the Medicaid program. States can’t drop poverty-level patients if they don’t pay premiums, charge people more than Medicaid rules allow, force patients to work or hunt for a job, or limit certain Medicaid benefits. These rules help make sure people actually get care, which is the fundamental goal of the expansion.

Ultimately, national health care reform is about better health for all Americans – including those with moderate and low incomes – and strengthening the health care system that serves all Americans. Ohio’s Medicaid expansion plan is doing well. Ohio should stay the course.

[1] Wendy Patton, “Medicaid expansion benefits Ohio,” October 2014 at http://www.policymattersohio.org/wp-content/uploads/2014/10/Medicaid.pdf

[2] See Nakela Cook et al. “Access to Specialty Care and Medical Care Services in Community Health Centers.” Health Affairs, V.26, no. 5 (2007): 1459-1468 http://content.healthaffairs.org/content/26/5/1459/T2.large.jpg.

See also United States Government Accountability Office, Report to the Secretary of Health and Human Services, “Medicaid: States Made Multiple Program Changes, and Beneficiaries Generally Reported Access Comparable to Private Insurance.” 11/2012. (GAO-13-55.) http://gao.gov/assets/650/649788.pdf

[3] A national study comparing quality of hospital care between patients with Medicaid and those with private insurance found no difference between Medicaid and private pay for two of three medical conditions studied for Ohio and only a one-percentage-point difference for the third. Ohio’s scores were always above the national Medicaid average. William Hayes, Op. Cit., (drawing on Joel S. Weissman, Christine Vogeli, and Douglas E. Levy. “The Quality of Hospital Care for Medicaid and Private Pay Patients.” Medical Care. 5/2013; 51:389-395.)

[4] Cleveland ranked 4th among the top ten most unbanked big cities in the nation; Cleveland and Cincinnati both made the top 10 list in terms of cities with the largest numbers of census tracts with high proportion of unbanked households. Corporation for Enterprise Development at http://cfed.org/assets/pdfs/Most_Unbanked_Places_in_America.pdf. The Federal Deposit Insurance Corporation found 7.8 percent of households in Ohio were unbanked in 2013. https://www.economicinclusion.gov/surveys/2013household/documents/tabular-results/2013_banking_status_Ohio.pdf

[5] Virginia Department of Medical Assistance Services memo, 5/15/2002; see also, L. Summer & C. Mann, “Instability of Public Health Insurance Coverage for Children and Their Families: Causes, Consequences, and Remedies,” The Commonwealth Fund (June 2006). Cited in Tricia Brooks, Handle with Care: How Premiums Are Administered in Medicaid, CHIP and the Marketplace Matters, Georgetown University Center for Families and Children at http://www.healthreformgps.org/wp-content/uploads/Handle-with-Care-How-Premiums-Are-Administered.pdf

Tags

2015Budget PolicyMedicaidWendy PattonPhoto Gallery

1 of 22