Tax breaks expand in state budget

September 16, 2015

Tax breaks expand in state budget

September 16, 2015

Contact: Zach Schiller, 216.361.9801

By Zach Schiller

Executive summary

The new state budget adds significant new tax breaks to a tax code that already included 128 of them, worth more than $8 billion a year. At the same time, the General Assembly turned down a number of proposals to limit or repeal some existing tax exemptions and credits. This leaves the state with more tax breaks, totaling hundreds of millions of dollars a year, than the number when the year began. All but a small portion of this drain on revenue comes from an expansion of a tax break to business owners that is unlikely to generate significant new jobs, just as an earlier form of this deduction did not do so.

The new state budget adds significant new tax breaks to a tax code that already included 128 of them, worth more than $8 billion a year. At the same time, the General Assembly turned down a number of proposals to limit or repeal some existing tax exemptions and credits. This leaves the state with more tax breaks, totaling hundreds of millions of dollars a year, than the number when the year began. All but a small portion of this drain on revenue comes from an expansion of a tax break to business owners that is unlikely to generate significant new jobs, just as an earlier form of this deduction did not do so.This report reviews new tax exemptions, credits and deductions approved as part of the budget. These breaks are known as “tax expenditures” because they are in effect another form of state spending, just spending done through the tax code. “Tax expenditures result in a loss of tax revenue to state government, thereby reducing the funds available for other government programs,” the Ohio Department of Taxation noted in its 2013 tax expenditure report. “In essence, a tax expenditure has the same fiscal impact as a direct government expenditure.”

By far the largest new tax break in the budget is an expanded deduction for income from owners of passthrough entities – businesses such as partnerships and S Corporations whose income is taxed when it passes through to its owners. The Kasich administration has estimated the cost of that expansion in Fiscal Year 2017 at $558 million. The initial tax break, approved in 2013, did not produce overall job gains for the state, or a significant increase in employment at small businesses that were hiring employees for the first time. Business owners in general invest because there is a growing market for their products or services, not because they have more cash in their wallets. The average tax savings in 2014 from the deduction was about $1,050, with most claiming far less than that. As a result, it’s not surprising that many business owners didn’t bother claiming it at all—the taxation department spent $38,000 informing 130,000 such owners they were eligible for it but hadn’t claimed it.

A number of others were approved. These included:

- A break on the state’s main business tax for companies located in a suburban Columbus business park that are in the same supply chain making “a personal care, health, or beauty product or an aromatic product, including a candle.” This carve-out, which is retroactive, favors such companies over similar ones elsewhere, including those in Ohio. The Office of Budget and Management (OBM) estimated the cost at $5 million this year and $3 million in Fiscal Year 2017.

- A sales-tax exemption covering sanitation services provided to meat slaughtering or processing operations simply because they are necessary to comply with federal meat safety regulations. Estimated FY 2017 cost: $2.6 million.

- A sales-tax exemption on rental vehicles that car dealers provide while repairing customer vehicles, if the cost of the rental vehicle is being reimbursed. Estimated cost: $2.7 million.

- Expansion of a local property tax break that covers fraternal organizations like the Masons and the Moose if the property is used to provide educational or health services on a nonprofit basis.

Not all of the changes in tax breaks were revenue losers. The General Assembly means-tested four income-tax credits, including the retirement income credit and the $50 senior credit, so that only those taxpayers with income below $100,000 are eligible for them. The narrowed eligibility for those two is expected to generate $28.4 million in FY 2017. The legislature also overhauled the state’s rules for when sales or use tax must be collected, including a requirement that online retailers must collect tax if they use Ohio web sites to refer potential customers.

A missed opportunity: No review for tax breaks

Ohio still has no thorough, regular review of its tax expenditures, even though they would amount to a sizeable share of state tax revenues if they didn’t exist. Legislators rejected language in the Senate budget bill that would have required such a review, the second time that has happened in four years, as well as Gov. Kasich’s proposal for a one-time examination of tax expenditures.

That represents a missed an opportunity to review the spending the General Assembly has authorized through the tax system.

However, in a positive step, it did provide for a review of the state’s tax credits. And even as the budget was being approved, the House unanimously passed House Bill 9, which calls for a permanent committee to review all tax expenditures every eight years. While this bill could be strengthened, most notably by including automatic expiration for all existing tax expenditures, it deserves approval by the Senate. Just as legislators make decisions on state expenditures, all spending through the tax code also should be regularly reviewed. Instead, the General Assembly is approving additional tax expenditures.

Introduction

The new state budget adds significant new tax breaks to a tax code that already included 128 of them, worth more than $8 billion a year, as counted by the Ohio Department of Taxation. At the same time, the General Assembly turned down a number of proposals to limit or repeal certain existing tax exemptions and credits. While some special-interest provisions included in earlier versions of the budget did not find their way into law, this still leaves the state with more tax breaks, totaling hundreds of millions of dollars a year, than when the year began.This report reviews new tax exemptions, credits and deductions, known as “tax expenditures” because they are in effect another form of state spending, just spending done through the tax code. “Tax expenditures result in a loss of tax revenue to state government, thereby reducing the funds available for other government programs,” ODT noted in its 2013 tax expenditure report. “In essence, a tax expenditure has the same fiscal impact as a direct government expenditure.”[1]

Ohio still has no thorough, regular review of its tax expenditures, even though they would amount to a sizeable share of state tax revenues if they didn’t exist. Legislators rejected language in the Senate budget bill that would have required a review, the second time that has happened in four years. They also rejected Gov. Kasich’s proposal for an examination of tax expenditures.

The General Assembly approved a one-time review of tax credits. This is a move in the right direction. There are 34 tax credits worth close to $1 billion a year.[2] And there is some prospect for a broader review, since the House of Representatives unanimously passed House Bill 9, which would set up a permanent committee to review all tax expenditures every eight years. But as of now, most tax expenditures remain unexamined. Just as legislators make decisions on what the state should spend, spending through the tax code also should be regularly reviewed. Instead, the General Assembly is approving additional tax expenditures.

A huge business tax break

By far the largest addition to tax expenditures in the new budget is the expansion of a tax break for business income first approved two years ago. When fully implemented next year, this will exempt the first $250,000 of business income from the income tax, while setting a 3 percent rate for all such income over that amount. The Kasich administration has estimated the cost of that in Fiscal Year 2017 at $558 million.[3] Including the existing deduction, which excluded half of the first $250,000 in such income from tax, this could cost more than $800 million a year. That likely will make it the second-largest tax break in the tax code.[4] It covers income from entities such as partnerships, limited liability companies, sole proprietorships, and S Corporations, which are known as “passthrough entities” because their profits are taxed under the income tax when they pass through to owners.

Sold as a job creator, the existing deduction hasn’t produced. Overall job growth in Ohio continues to trail the national average; in the 25 months since the tax break was enacted, the United States has gained 5.8 million jobs, or 4.3 percent, compared to Ohio’s gain of 142,300, or 2.7 percent. In fact, Ohio job growth in those 25 months trailed that of the state in the previous 25-month period, which was 3.4 percent. And hiring by new companies of their first employees, tracked by the U.S. Bureau of Labor Statistics, has not quickened. In the first three quarters of last year, the number of employees added by new businesses adding employees for the first time was below the same period in 2012 or 2013, and down 29 percent from that period in 2004, a decade earlier.

There is no reason to think that such tax cuts would be an effective job creation strategy. Most owners of such passthrough entities employ no one but themselves. While data from the Taxation Department shows there are more than 1 million pass-through-entity businesses in Ohio, fewer than 300,000 private companies pay unemployment tax. This essentially means that most of them employ no one, since nearly all companies are required to pay this tax for each employee.[5] Many are passive owners, as Michael Mazerov of the Center on Budget and Policy Priorities noted in 2013 testimony to the Ohio House Finance Committee,[6] and their businesses serve a local market and plan to keep it that way. The small minority of new business start-ups that engage in real innovation likely are plowing all of their resources into investing in the business, and may therefore have less profit than the average small business. And business owners in general invest because there is a growing market for their products or services, not because they have more cash in their wallets.[7]

Most business owners won’t get anywhere close to enough from the new break to hire a permanent employee. The average tax savings in 2014 from the deduction was about $1,050; for the 72 percent of those business owners who claimed it with deductions of $20,000 or less, the average was $246.[8] Perhaps it’s not surprising that so many business owners didn’t bother claiming it—the taxation department spent $38,000 mailing post cards to 130,000 such owners to inform them that they were eligible for it but hadn’t claimed it.[9]

Yet at the same time, the expansion of this tax break will especially benefit owners with the most income. The existing deduction, which was increased to 75 percent just for 2014, went heavily to owners with the largest amount of such income. The 6 percent of the total using it who claimed at least a $100,000 deduction accounted for almost 42 percent of the total claimed.[10]

Nor is it just a “small business” tax break, as it is often called. According to IRS data, there were 4,400 Ohio passthrough entities with 2011 gross receipts of $10 million or more. Though these companies accounted for less than half of one percent of the state’s 1.05 million passthrough businesses, they generated $12.5 billion in income. That was close to half the total for all such entities in the state, and more than the collective total of all passthroughs with receipts of $2 million or less.[11] Owners of these larger entities will benefit most from the new 3 percent flat rate on business income over $250,000.

Ironically, in approving this expanded tax break, legislators actually increased taxes for 2015 on some business owners. This year only, the language of the bill calls for the 3 percent flat rate to apply to 25 percent of the first $250,000 in business income that can’t be deducted. That’s a higher rate than what many business owners have been paying under Ohio’s graduated income tax. The General Assembly inadvertently demonstrated how such a progressive tax is beneficial to lower-income Ohioans with this move, though it is now considering bills to “correct” it.[12]

Other, smaller tax breaks

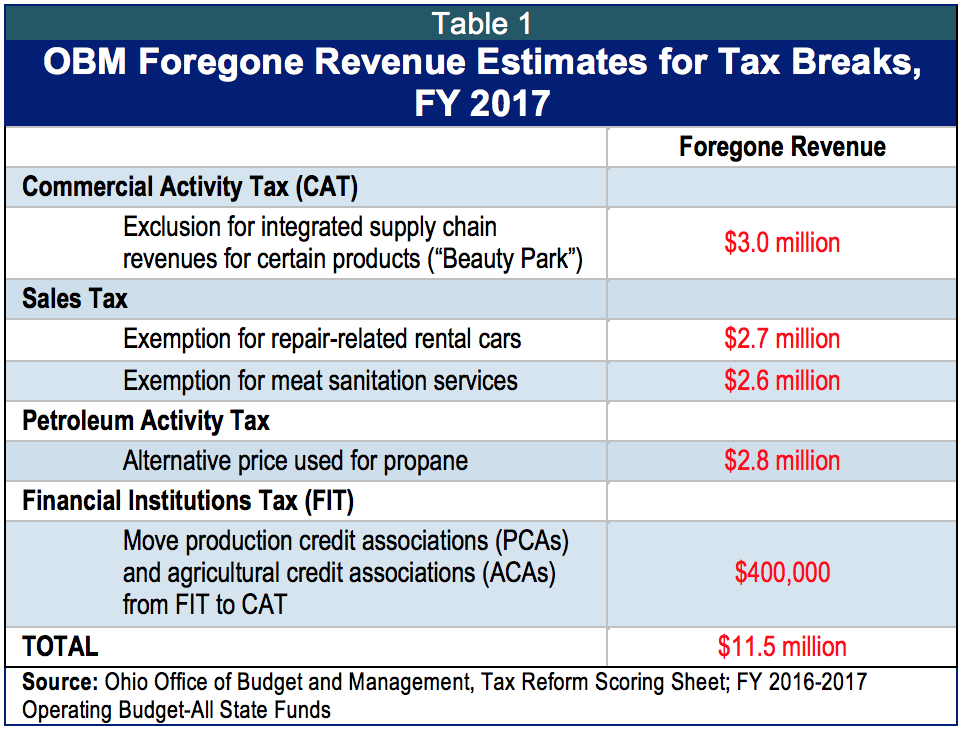

The expansion of the tax break for business income is much larger than any other new or expanded tax break. According to the Office of Budget and Management, five other tax breaks approved by the General Assembly will cost a total of $11.1 million in Fiscal Year 2017. Each was added by the Senate, which inserted a host of new tax breaks into the bill, not all of which remained in the final version. Table 1 below lists these new tax expenditures:

The largest of the five, valued by OBM at $5 million this fiscal year and $3 million in FY17, is a tax break for a company that delivers parts or inventory that will become part of “a personal care, health, or beauty product or an aromatic product, including a candle” to another company in the same supply chain. The two companies must “systematically collaborate and coordinate business operations with a retailer on the flow of tangible personal property from material sourcing through manufacturing, assembly, packaging and delivery to the retailer…”[13] They also must be in a 400-700 acre commonly owned area in New Albany, outside Columbus. The exemption means that sales by one such vendor to another won’t be taxed under the Commercial Activity Tax, the state’s main business tax, and applies retroactively to July 1, 2011.

This is a classic special-interest exemption—and making it apply even in past years is especially hard to justify.[14] Though narrowed somewhat in the final version of the bill to exclude equipment sales and receipts to a retailer, it provides an advantage to individual firms over similar companies, including those operating in Ohio. Such carve-outs reduce the base of the tax and do not serve the public interest. This one was opposed by several groups, including the Ohio Manufacturers Association, which has a history of opposing carve-outs to the Commercial Activity Tax.

One of the sales-tax exemptions covers rental vehicles that car dealers provide while repairing customer vehicles, if the cost of the rental vehicle is being reimbursed. Gov. Kasich vetoed a similar exemption in another bill earlier this year. “This amendment creates a loophole that will result in significant refunds and will subject similar transactions to different tax treatment without sufficient justification,” he said in his veto message.[15]

Another new sales-tax exemption covers sanitation services provided to meat slaughtering or processing operations if they are necessary to comply with federal meat safety regulations beginning Oct. 1.[16] Ohioans might be surprised to learn that meat processors will receive this exemption simply because they are doing what federal law requires. Imagine if you got a tax break every time you followed the law.

Another provision in the budget bill allows production credit associations and agricultural credit associations, which make loans to farmers and some others, to be taxed under the Commercial Activity Tax instead of the Financial Institutions Tax. It is retroactive to Jan. 1, 2014, when the FIT was established, and is described in the bill as “remedial in nature” and “intended to clarify the law as it existed” previously.[17] It is unclear whether or not this was an oversight when the FIT was established, replacing other taxes on financial institutions.

Up until now, the market price of diesel fuel has been used to calculate taxable gross receipts under the Petroleum Activity Tax not only for diesel but for other motor fuels besides gasoline, such as kerosene, biodiesel and propane. The bill calls for the price of propane to be used instead of diesel for propane receipts, reducing tax receipts.[18]

The General Assembly also approved some other changes in tax credits and exemptions. It once again made changes in two of the state’s key economic development incentive programs, the job creation tax credit (JCTC) and the job retention tax credit (JRTC). It changes their computation so they will be based on employee payroll, rather than the employee income-tax the employer withholds. As the LSC noted in an analysis of the bill, this “prevents a reduction in the credit amount due to declining Ohio income tax rates.”[19]

The budget bill also allowed companies that had been awarded these credits to ask for the terms to be adjusted retroactively, so they increase or decrease to take into account the income-tax rate changes approved since June 29, 2013. Since the income tax has been cut since then, this means increases in such credits. For those agreements approved in 2014 or 2015, the company needs approval of the state Tax Credit Authority. For agreements dating to before 2014, the Tax Credit Authority is required to compute an adjustment in the credits based on the changes in income-tax rates.

The additional cost of these changes increasing credits to take into account Kasich-era income-tax cuts is not clear. The LSC said only that this and other provisions involving the two credits would potentially reduce revenue from a number of different taxes.[20] Neither the state budget office nor the department of taxation has estimated the cost of the JCTC provisions, and the Development Services Agency says that the changes would be revenue-neutral.[21]

The General Assembly also approved a number of other changes in the JCTC and JRTC as part of the budget. It removed a cap on the JCTC that had existed under the prior law. It also authorizes tighter enforcement of conditions for the two credits, allowing the Tax Credit Authority to require the company to refund all or part of the tax credit if it doesn’t substantially meet the job creation, payroll, or investment requirements in the tax credit agreement. And it required the development agency to make available an estimate of the total revenue foregone as a result of tax incentives approved by the Tax Credit Authority within 30 days of that approval.

Another provision authorizes a new deduction from the Petroleum Activity Tax allowing motor fuel suppliers to avoid paying the tax on additives sold for blending with motor fuel if the tax already has been paid on that product. The LSC described this deduction as creating a potential revenue loss of uncertain magnitude. It explains: “Essentially, the deduction ensures that the sale of blend stocks incorporated into motor fuel is subject to the PAT only once, i.e. the blend stock is taxed at its first point of sale, but not a second time when it is incorporated into and sold as blended motor fuel.”[22] OBM sees this change as having minimal impact.[23]

The General Assembly also revised some other tax breaks aimed at stimulating economic development. It made some changes in the state’s New Markets Tax Credit, including how it is calculated and who can receive it, but left the $10 million annual cap unchanged. This program is supposed to encourage investments in low-income communities. It extended special treatment for another two years for some owners of a historic preservation tax credit certificate to claim the credit under the Commercial Activity Tax if they can’t claim it under another credit. When this was initially approved a year ago, the taxation department estimated that it would cost $39 million in Fiscal Year 2015, with some residual in Fiscal Year 2016.[24] LSC said that this provision in the recent budget bill would cause a GRF revenue loss “potentially in the millions.” In addition, a committee authorized by the budget bill is to study the effectiveness of this credit by Oct. 31, 2016, and whether to convert it to a refundable credit or a grant program.[25]

It also created a new tax break for a company, apparently in New Albany, that uses at least 7 million kilowatt hours a year of wind energy. According to an article in Gongwer News Service, the break is aimed at a company that is considering building a data center in that city.[26] The break comes in the form of a tax reimbursement to the local government, which in turn would provide the company with an amount equal to the kilowatt-hour excise tax paid on the wind-generated energy it received. This special payment was lumped together with the bill’s tangible personal property tax reimbursement scheme, although it has nothing to do with that. The LSC said that “reimbursements would be somewhat higher” because of this provision, without providing an exact estimate; OBM identified the impact as minimal.[27] The budget bill also extended by five years an existing local property tax break for renewable energy projects, and renewed the enterprise zone local property tax abatement program for another two years.

A number of other tax-break provisions affect local taxes.[28] For instance, the General Assembly broadened a local property tax break that covers fraternal organizations like the Masons and the Moose if the property is used to provide educational or health services on a nonprofit basis.[29] According to Gongwer, “Ohio Department of Taxation spokesman Gary Gudmundson said the agency has tallied 1,332 applications for the property tax exemption from fraternal organizations since the bill passed less than two years ago. Before the law passed, total applications for property tax exemptions around the state totaled 3,283, he said. "So this is a pretty sizable jump in the population of taxpayers asking for property tax exemptions," he said.”[30] The Legislative Service Commission found that it may increase the revenue loss for school districts and local governments, without estimating an amount.[31] Other provisions made changes in the municipal income tax.[32] Policy Matters Ohio has reviewed elsewhere the effects of key budget bill provisions on local governments, which have not seen the restoration of major cuts made earlier, and of further cuts in state tax reimbursements on local human service levies.[33]

Not all revenue losers

Not all of the tax changes were revenue losers.[34] The General Assembly means-tested four income-tax credits, including the retirement income credit and the $50 senior credit, so that only those taxpayers with income below $100,000 will be eligible for them.[35] OBM estimated that that will generate $24.4 million and $3.9 million, respectively, in FY2017.[36] According to data from the state taxation department, the means-testing would have excluded 14 percent of the 901,269 filers who claimed the retirement income credit in 2011, and 10.4 percent of those who claimed the senior credit.[37] Limiting these credits is a worthwhile step. It will make the tax system fairer and is financially responsible, as it preserves revenue as the population ages.[38] Unfortunately, the General Assembly rejected Gov. Kasich’s proposal to do with the same with the deduction for Social Security income, a more significant step.

The legislature also overhauled the state’s rules for when sales or use tax must be collected (Use tax is equivalent to the sales tax, and is supposed to be collected on out-of-state purchases of property or services that are used in Ohio).[39] Among other things, it called for the tax to be collected if a company has an affiliate selling similar goods and doing business under similar trademarks. It also means the tax has to be collected if a company pays one or more Ohio residents to refer potential customers, if such sales add up to more than $10,000 over the year. This referral can be through a link on a web site, an in-person presentation, or through telemarketing. It is sometimes called “click-through nexus.”[40] The LSC estimated that these provisions would increase state revenue by “several millions of dollars a year.” It also would increase revenues from sales taxes levied by counties and transit authorities, the LSC said.[41]

This provision could help level the playing field for some Ohio retailers that previously had to compete against out-of-state, online retailers that did not have to collect the tax. Though the tax is due on their sales here, many don’t have to collect it because a U.S. Supreme Court decision said retailers can’t be required to do so if they don’t have a physical presence in the state. Gov. Kasich vetoed a similar provision when it was included in the budget two years ago, but did not do so this time. Perhaps one reason is that in June, the largest online retailer, Amazon.com, began collecting sales tax in Ohio when it announced it would be opening facilities here, which would have forced it to collect the tax.

Leaving loopholes untouched

The General Assembly passed up an opportunity to reduce some unproductive tax breaks. In his initial budget plan, Gov. Kasich proposed reductions in a number of credits and exemptions, including:

- Eliminating the credit that sellers of beer, wine and mixed beverages get for paying their alcoholic beverage tax a few weeks in advance[42];

- Limiting the amounts retailers can receive for collecting the sales tax, known as the vendor discount. Most states either have no discount at all or cap the amount, ensuring that big retailers do not reap a windfall. Indeed, Tax Commissioner Joe Testa said in testimony that Ohio’s 0.75 percent discount “essentially functions as a profit center” for big-volume retailers.

- Cutting the sales-tax exemption for trade-ins of used cars and boats in half, and

- Repealing the 2.5 percent discount that distributors of cigars, chewing tobacco and other tobacco products get for timely payment of their taxes. “It shouldn’t be necessary to reward businesses for paying their tax on time,” as Testa noted. [43]

Gov. Kasich vetoed a number of provisions the General Assembly had approved that would have created or expanded a number of tax breaks. These included, among others, a reduction in the Petroleum Activity Tax for dyed diesel fuel used by railroads, an income-tax deduction for dentists and dental hygienists for free services provided under a “Hope for a Smile” program, automatic income-tax reductions tied to the costs of provisions that a governor vetoes, a tax amnesty, a reduction in assessment values for new water-works property and a provision to cut taxes on property used by utilities to generate electricity and shift it onto transmission and distribution properties. Most of these vetoes appropriately scuttled unneeded special-interest breaks. However, the governor also vetoed provisions the General Assembly had included to protect school districts from reductions in tax reimbursements, costing them tens of millions of dollars in needed aid.

Conclusion and Recommendations

The two-year Ohio state budget contains new tax breaks costing hundreds of millions of dollars a year, the vast bulk of that from an unproductive expansion of a business tax break that has not proven its worth. While a handful of existing tax breaks were means-tested and some online retailers could start collecting use tax under the bill, none of the state’s 128 tax expenditures were eliminated, unlike in the biennial budget two years ago.[44] The General Assembly missed an opportunity to review the spending that it has authorized through the tax system, or to authorize a full-scale, regular review of the 128 exemptions, credits and deductions in the tax code.

The expansion of tax breaks, especially the big one for business owners, reduces state revenue that should go instead for a host of unmet needs. Among others, these include tearing down or rehabilitating the thousands of vacant and abandoned homes across Ohio; providing adequate protection for Ohio’s neglected and abused elderly and children; helping more families pay for child care, so the parents can work; boosting our support for public transit, which ranks below that of South Dakota; restoring aid to local governments hammered by state reductions; and reinstating need-based aid for college students.

In a positive step, the General Assembly did provide for a review of the state’s tax credits. And even as the budget was being approved, the House unanimously passed House Bill 9, which calls for a permanent committee to review all tax expenditures every eight years.[45] While this bill could be strengthened, most notably by including automatic expiration for all existing tax expenditures, it deserves approval by the Senate. Just as legislators make decisions on state expenditures, all spending through the tax code also should be regularly reviewed.

The author would like to acknowledge Policy Matters Ohio intern Andrew Slivka for research help he provided for this report. We would like to thank the Center on Budget and Policy Priorities, the Saint Luke’s Foundation, George Gund Foundation, and the Ford Foundation for their generous support that allows us to do this analysis.

[1] Governor John R. Kasich, Ohio Department of Taxation, The State of Ohio Executive Budget, Fiscal Years 2014-2015, Tax Expenditure Report, p. 1, available at http://1.usa.gov/13EVGI3.

[2] Ibid.

[3] Ohio Office of Budget and Management, Tax Reform Scoring Sheet; FY 2016-2017 Operating Budget-All State Funds. The Legislative Service Commission estimated the FT2017 cost at $490 million.

[4] A number of observers also have noted that the tax break could result in greater tax avoidance, as some who are now paid as employees shift to become independent contractors and don’t have to pay tax on the first $250,000 in income.

[5] See Zach Schiller, “Business Tax Break Proposal: Costly, Unfocused and Unlikely to Bring New Jobs,” Policy Matters Ohio, Apr. 9, 2015, p. 2, at http://www.policymattersohio.org/business-tax-april2015

[6] Mazerov, Michael, “Testimony to House Finance & Appropriations Committee on HB 59 Income Tax Plan,” March 19, 2013, at http://www.policymattersohio.org/mazerov-mar2013

[7] Ibid.

[8] Policy Matters Ohio calculations from data provided by the Ohio Department of Taxation, Small Business Deduction Report, June 3, 2015. The department previously estimated that on average, the business owners had paid a tax rate of about 4.5 percent.

[9] Joe Testa, Tax Commissioner, Ohio Department of Taxation, comments during testimony to the Senate Ways & Means Committee, Apr. 29, 2015, and email from Gary Gudmundson, Ohio Department of Taxation, July 17, 2015

[10] Calculated from Ohio Department of Taxation, Small Business Deduction Report, Tax Year 2014, Report run June 3, 2015.

[11] Joe Testa, Tax Commissioner, Ohio Department of Taxation, Testimony to the House Finance Committee, Feb. 12, 2015, Attachment B: Pass-through Entities by Size of Gross Receipts, p. 19, available at http://www.ohiohouse.gov/committee/finance

[12] Policy Matters Blog, “The Benefits of a Graduated Tax,” July 20, 2015, at http://www.policymattersohio.org/blogpost-tax-july2015 explains how the graduated rate structure of Ohio’s income tax means that lower-income residents pay less than they would under a flat tax. Ironically, under the approved provisions for the tax break, some business owners found themselves in the same position this year as lower-income Ohioans would if the ongoing income tax was converted into a flat-rate tax. The bills with the proposed change are Senate Bill 208 at https://www.legislature.ohio.gov/legislation/legislation-documents?id=GA131-SB-208 and House Bill 326 at https://www.legislature.ohio.gov/legislation/legislation-summary?id=GA131-HB-326

[13] House Bill 64, pp. 2350-51

[14] See Policy Matters Blog, “The Butcher, the Baker, the Candlestick Maker…and the Golf Course Operator,” June 16, 2015, at http://www.policymattersohio.org/blogpost-taxbreaks-june2015

[15] State of Ohio, Executive Department, Office of the Governor, Veto Messages, Statement of the Reasons for the Veto of Items in Substitute House Bill 53, April 1, 2015, p. 2, at https://www.legislature.ohio.gov/Assets/AdditionalDocuments/HB-53-veto-message-2.pdf. Kasich said in the message that “a dealer who provides a vehicle from its inventory for the same courtesy transportation must pay use tax.”

[16] Legislative Service Commission, Final Analysis, Am. Sub. H.B. 64, 131st General Assembly (As passed by the General Assembly), p. 517, at http://www.lsc.ohio.gov/budget/agencyanalyses131/final/15-hb64-131.pdf

[17] 131st General Assembly, Amended Substitute House Bill 64, Section 757.140, p. 2861.

[18] Legislative Service Commission, Final Analysis, Am. Sub. H.B. 64, p. 522

[19] Ibid, p. 531

[20] Legislative Service Commission, Comparative Document, Department of Taxation, p. 61

[21] Emails from Gary Gudmundson, Ohio Department of Taxation, and John Charlton, Office of Budget and Management, Sept. 14, 2015, and Todd Walker, Development Services Agency, Sept. 15, 2015.

[22] Ibid, p. 541.

[23] Email from John Charlton, Office of Budget and Management, Sept. 4, 2015

[24] Schiller, Zach, “Cuts and Breaks: Tax Changes in the Mid-Biennium Review,” Policy Matters Ohio, July 2, 2014, p. 8, at http://www.policymattersohio.org/cuts-and-breaks-mbr-jul-2014

[25] HB 64, Section 757.50(A), p. 2857, at https://www.legislature.ohio.gov/legislation/legislation-documents?id=GA131-HB-64

[26] Gongwer News Service, “Budget Extends Renewable Tax Break, Creates Limited Incentives for Wind Power,” Volume 84, Report 130, July 8, 2015.

[27] Legislative Service Commission, Comparative Document, Department of Taxation, p. 51, at http://www.lsc.ohio.gov/fiscal/comparedoc131/en/tax.pdf and Charlton email, op.cit., Sept. 4, 2015.

[28] Local tax changes included continued favorable tax treatment for material that is dredged from Buckeye Lake, authorizing a township with at least 15,000 people to extend an existing tax increment financing resolution for another 15 years, and tax forgiveness on a submerged land lease held by a municipal corporation. The General Assembly also permitted a number of specific revenue-raising measures at the local level, such as lengthening the maximum term of property taxes used to operate a cemetery, and allowing for higher lodging taxes for an Erie County sports park, for Delaware County to make improvements where the agricultural society conducts fairs or exhibits, and for Warren County to build sports facilities.

[29] Under previously existing law, annual gross income from renting the property to others may not exceed $36,000.

[30] Gongwer News Service, “House Budget Expands Fraternal Groups’ Property Tax Exemption,” May 13, 2015

[31] Legislative Service Commission, Comparative Document, Department of Taxation, p. 44

[32] In a June 23 letter to Gov. Kasich asking that he veto certain provisions in the budget bill, officials from the Ohio Municipal League said, “Further changes are being proposed for the administration of the municipal income tax that were not vetted through the legislative process, neither through committee hearings or distribution of the included changes to municipal tax officials or representatives of municipal government. These include changes to extension for municipal income tax returns; taxation of publicly traded partnerships; changes to municipal taxation of foreign income; new procedures for former municipal income taxpayer to submit affidavits; changes to municipal tax sharing with school districts; and language related to the Net Operating Loss (NOL) Carry Forward provision that was tremendously ambiguous in previous tax reform legislation.” Susan J. Cave, executive director, and James A. Bodenmiller, president of the executive board, Ohio Municipal League, Letter to the Hon. John Kasich, June 23, 2015, at http://www.omlohio.org/131st%20Gen%20Ass/Budget%20Bill%20Veto%20Request%20.pdf

[33] See Wendy Patton, Policy Matters Blog, “State budget hammers local governments – again,” Aug. 24, 2015, at http://www.policymattersohio.org/blogpost-localgovt-aug2015 and “Health and human services lose out,” May 4, 2015, at http://www.policymattersohio.org/blogpost-taxcuts-may2015

[34] The largest revenue increase in the budget was the 35-cent-a-pack boost in the cigarette tax. That increase was included in a previous Policy Matters Ohio report that reviewed the biggest tax measures in the budget. These included a 6.3 percent cut in income-tax rates. See Zach Schiller, “Well-off are Winners in Ohio Tax Plan,” Policy Matters Ohio, June 26, 2015, at http://www.policymattersohio.org/taxplan-june2015

[35] The other two that were means-tested at the same level are smaller lump-sum credits.

[36] The LSC estimated that means-testing all four would generate $25.5 million in FY17. See LSC Comparative Document, Department of Taxation, p. 9.

[37] Email from Gary Gudmundson, Ohio Department of Taxation, Feb. 26, 2015

[38] While this means-testing was worthwhile, it merely reduced the windfall in the tax plan for Ohio’s wealthiest, which should have been used instead to support vital public services. See “Well-off are Winners in Ohio Tax Plan.”

[39] While these changes generally tightened up requirements for collection of such taxes, they also contained a provision that might allow some companies that previously would have bene covered to avoid collecting them. If a company that has a warehouse in Ohio is able to show that it isn’t used to deliver products to Ohio customers, for instance, it could avoid the requirement.

[40] Legislative Service Commission, Final Analysis, Am. Sub. H.B. 64, 131st General Assembly (As passed by the General Assembly), p. 514.

[41] Legislative Service Commission, Comparative Document, Department of Taxation, p. 22. By contrast, the Office of Budget and Management identified the impact as minimal (see Charlton email, op. cit., Sept. 4, 2015)

[42] See Policy Matters Blog, “Brewer Crying in its Beer Over Losing Discount for On-Time Tax Payments,” April 13, 2015, at http://www.policymattersohio.org/blogpost-beer-april2015

[43] Testa, op. cit., Testimony to the House Finance Committee, pp. 11 and 15.

[44] Schiller, Zach, “Tax Breaks Grow in New Ohio Budget,” Policy Matters Ohio, Aug. 8, 2015, at http://www.policymattersohio.org/tax-breaks-aug2013

[45] The Senate Ways & Means Committee also held a series of hearings on tax expenditures while senators were waiting for the House to approve the budget bill.

Tags

2015Tax ExpendituresTax PolicyZach SchillerPhoto Gallery

1 of 22