Testimony: Unemployment bill should be spiked

December 02, 2015

Testimony: Unemployment bill should be spiked

December 02, 2015

Contact: Zach Schiller, 216-361-9801

Good morning, Chairman Hackett, Ranking Member Bishoff and members of the committee. My name is Zach Schiller and I am research director at Policy Matters Ohio, a nonprofit, nonpartisan organization with the mission of creating a more prosperous, equitable, sustainable and inclusive Ohio. Thank you for the opportunity to testify today regarding House Bill 394.

Ohio needs to come up with a solution to adequately finance its unemployment compensation (UC) system. Unfortunately, House Bill 394 is not the right solution.First, it is not a balanced package. All of the savings comes from unemployed workers – in fact, more than all, since the bill will result in substantial tax cuts.

Second, it is not a true solvency package. According to information provided by the bill sponsor, the system will remain more than $1.3 billion short of the new minimum safe level in 2025 – and that relies on the unrealistic assumption that there will be no recession for another 10 years.

Third, it misdiagnoses the reasons for Ohio’s solvency problem. The key reason why our fund went broke is that it was underfunded for many years. Employer taxes in Ohio have been below the national average. Yet the bill would not produce more revenue, but less – considerably less.

Fourth, the bill’s reductions in benefits, and access to benefits, would take Ohio well outside the mainstream. They would make our UC program among the most restrictive in the country. No other state has imposed the barriers to access contained in House Bill 394. And it inexplicably would reverse a law protecting older Ohioans approved unanimously by both houses of the General Assembly just eight years ago. These changes will disproportionately negatively impact regions with higher levels of unemployment and slower job growth, such as our Appalachian counties and many of our cities.

Let’s take these points one by one.

Not a balanced package

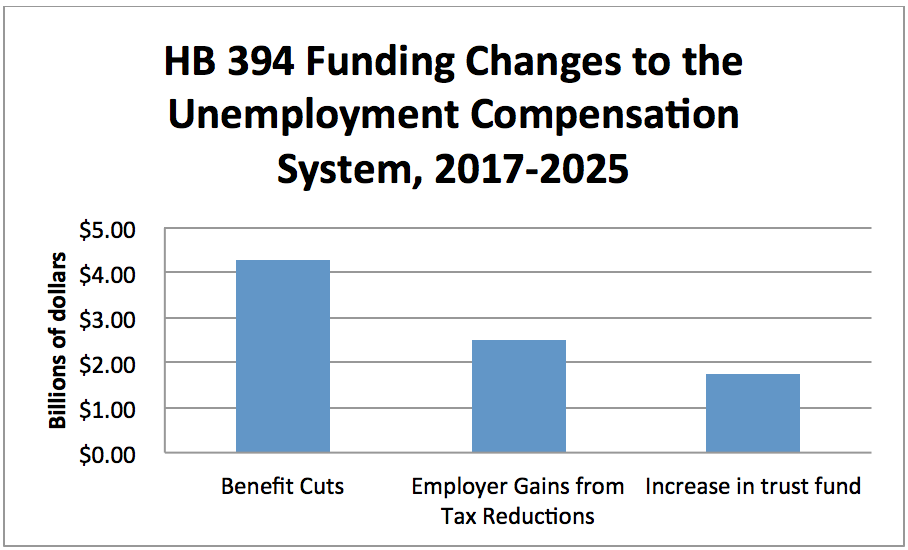

There are a lot of moving parts to the unemployment compensation system. But in the end, solvency of the system depends on how much in benefits is paid out, and how much in taxes is paid in. According to estimates by the Ohio Department of Job and Family Services used by the bill sponsor and by the Legislative Service Commission in its analysis, benefit changes under House Bill 394 are projected to reduce UC benefits (the money going out of the system) by more than $460 million in 2017 alone, the first year they take effect. Estimated benefit cuts average $475 million annually between 2017 and 2025 and will add up to nearly $4.3 billion in benefit reductions by 2025. That amounts to a 41 percent cut in benefits over that timeframe.

Meanwhile, what will happen to employer taxes (the money coming into the system)? Much of the committee’s attention has focused on the increase in the wages being taxed, from $9,000 to $11,000, as long as the fund is below a safe level. But despite this increase, UC payroll tax revenues will fall well below both projected and historical levels in Ohio under the bill. This drop in revenue happens because benefit cuts are passed along as future tax reductions under Ohio’s UC experience rating mechanism. Simply put, since UC tax rates are based in large part upon benefit payouts in prior years, the drastic benefit cuts under the bill translate to overall tax reductions for employers starting in 2018, the year after UC cuts take effect. Under HB 394, both the money coming in and the money going out are reduced. Both average tax rates and overall revenue will fall, cutting revenue by an average of $313 million a year starting in 2018. That amounts to $2.5 billion between 2018 and 2025, or a 27 percent tax cut.

Figure 1 below shows the comparative “contributions” of unemployed workers and employers. These ODJFS estimates, the ones used by Rep. Sears for her testimony, show a complete lack of balance in contributions toward solvency by unemployed workers and employers, respectively. Workers will be asked to sacrifice so employers, as a group, can get substantial tax cuts.

Figure 1

Not a true solvency package

As the table indicates, the large employer tax cuts – amounting to more than half of the benefit cuts – substantially reduce the positive impact of the bill on the state’s UC trust fund. This means that it leaves the fund well short of the solvency that is the supposed goal. Under the bill, the fund would rise to an estimated $2.4 billion in 2025, slightly more than the solvency target under current Ohio law. But that would still be more than $1.3 billion or 35 percent below the safe level established under the bill, a threshold used by the U.S. Department of Labor.

However, these estimates assume there will be no recession between now and 2025. The current recovery since June 2009 to December 2015 is now 65 months long. According to the National Bureau of Economic Research, a private research group that declares when a recession begins and tracks the history of business cycles, the typical time between recessions since World War II has been 58.4 months. The longest recovery in U.S. economic history lasted 120 months. The bill’s assumption that this recovery will continue through 2025 without a recession adds over 100 months to the life of the current recovery. For HB 394 to get Ohio just slightly above our existing minimum safe level, which is clearly inadequate, we will need to have the longest period of economic growth in our national history. Under these unrealistic economic assumptions, HB 394 cannot be accurately perceived as a true solvency package.

Ohio employers are paying more federal tax than we typically do because we have not paid back our loan to the federal government. This bill does nothing to change that. ODJFS has estimated that under the current UC system we will pay off that loan in 2017. This means that even if the legislature takes no action on solvency, short of a severe recession beginning soon, Ohio employers will see a tax decrease after 2017. At that point, the additional federal taxes will go away — but not because of anything in the bill.

Misdiagnosing the problem

House Bill 394 is misdirected because it does not squarely address the main cause of the solvency problem. Overall tax collections in Ohio have left the trust fund far short of accepted solvency standards. Had Ohio employers paid the average national tax rate between 1996 and 2006, the state trust fund would have received an additional $1.7 billion. Ohio kept employer taxes below the national average, and the $2 billion that had been in the fund in 2000 was largely depleted before the 2007-2009 national recession; the U.S. Department of Labor rated Ohio as tied with Missouri for the third-least solvent fund in the country as the recession officially began in 2007.

State UC payroll taxes fall only upon the first $9,000 in wages (known as the taxable wage base). The taxable wage base was set at $9,000 in 1995. At that time, the taxable wage base covered 34 percent of total wages. By 2014, only 22.8 percent of all wages were subject to UC taxation under the $9,000 taxable wage base. This means that Ohio’s taxable wage base coverage of overall wages has fallen by one third (32.9 percent) since 1995. A low taxable wage base means that virtually any payroll tax mechanism will fail to adequately finance a UC program simply because not enough of the state’s wages are subject to tax.

Dr. Wayne Vroman, the leading economist on UC financing in the U.S., was commissioned by ODJFS in 2007 to help study the state’s UC financing. Dr. Vroman made projections and simulated the impact of solvency scenarios. He made expert solvency recommendations based upon those projections. He concluded that “…it would seem that most of the adjustments should involve enhancements to revenue since the benefit side of Ohio’s program has not undergone important changes in recent years. Benefit payments have grown as the economy has grown, but taxes have lagged economic growth.” Dr. Vroman recommended increasing and indexing the taxable wage base, making other changes in the structure of the tax, and freezing the maximum weekly benefit for three years, along with other changes. Dr. Vroman’s recommendations were ignored, and nothing was done.

Ohio’s taxable wage base would remain low even under the bill. The increase to $11,000 when the fund is below the minimum safe level would still leave Ohio well below the national average of $13,407, and the $14,046 it would be had it merely kept up with inflation since 1995. An $11,000 wage base would still be below that of 33 other states.

For the 12 months ended in June, Ohio’s state taxes as a share of wages were 0.62 percent. That was well below the national average of 0.79 percent – and also below every neighboring state.

Michigan was at 0.99 percent, and Pennsylvania, 1.27 percent. For the last five years and 16 out of the last 18, Ohio’s average state taxes have been below those for the nation as a whole.

Let’s put unemployment taxes in perspective. Ohio employers and companies across the nation are paying well under 1 percent of wages in state unemployment taxes. As of June, according to the Bureau of Labor Statistics, state unemployment insurance cost an average of 19 cents an hour for civilian workers, just 0.6 percent of the $33.19 in total compensation. If unemployment taxes were a major factor in attracting business, Ohio would have seen significant growth over the past decades, given our low taxes. That has not happened. By the same token, somewhat higher unemployment taxes are unlikely to cause economic losses.

Making Ohio an outlier

House Bill 394 takes aim at benefits, as if they are the cause of the system’s problems. That is incorrect. While a huge increase in benefit payout during the recession contributed to the debt, that was a result of high unemployment and very long spells of joblessness experienced all across the nation, not lucrative benefits. Ohio’s average benefit in the 12 months ended in June was $334.69, just 4.3 percent higher than the national average (and even this modestly higher average benefit is due in no small measure to state requirements that disqualify many lower-wage workers from qualifying). On an annual basis, our average benefit would amount to less than the federal poverty level for a family of three. Our overall benefit costs as a share of wages have been below the national average for the last five years, and for years prior to when the fund went broke were close to the U.S. average.

Last year, 208,622 Ohioans received unemployment benefits. That was the lowest number since 1973 – and fewer still are getting benefits this year. In fact, for many years, a smaller share of unemployed Ohioans has qualified for benefits than does jobless workers nationally. We require that workers earn more than in almost any other state in order to qualify. We deny benefits to jobless Ohioans seeking part-time work, even if they are seeking the same jobs they were laid off from, and even though their employers paid taxes on their wages. As ODJFS told the House committee studying the UC solvency issue last year, “Simply put, it is already more difficult to qualify for unemployment benefits in Ohio than in most states.”

Yet HB 394 would make it even more difficult. Right now, based on our unemployment rate, it would allow a maximum of just 12 weeks of benefits – last in the country, tied only with North Carolina. By contrast, 42 states offer 26 available weeks of UC in 2015, with two of these 42 having more than 26 weeks available. Overall, the bill would reduce the average number of weeks from an estimated 14.9 next year to below 10.

Basing the number of weeks of benefits available upon the state’s overall unemployment rate will create added challenges for claimants living in Ohio communities with high unemployment levels. Ohio is not one labor market. Unemployed workers in Monroe County, for instance, would be eligible for the same maximum 12 weeks of benefits as others all over Ohio were the bill in effect now. Yet its average unemployment rate according to ODJFS was over 10 percent during the first quarter of this year, the period used to set the maximum number of weeks for the second half of 2015. The comparable statewide rate was 5.7 percent. Many Appalachian counties and cities such as Cleveland and Youngstown have higher unemployment rates than the state as a whole, but unemployed workers there will be subject to the same maximum benefits as those elsewhere.

In addition to cutting maximum benefits, the bill would take extreme steps to further reduce access to UC, leaving Ohio out of the step with the nation. It would also:

- Require that laid-off workers must earn wages in at least three of the four calendar quarters in the prior year to have a valid UC claim. Right now, Ohio requires 20 weeks to qualify for some UC. Requiring wages in three quarters would hurt workers who are not employed throughout the year through no fault of their own. No other state imposes such a stringent requirement.

- Impose an additional waiting week, so that each time someone is laid off during a year, they would not receive benefits for a week when benefits would otherwise begin immediately. This would apply each time someone went back to work and was laid off, as long as they earned as much as their weekly benefit. Only North Carolina requires unemployed workers to serve more than one waiting week in a year.

- Restore the reduction (or offset) of weekly UC benefits when an otherwise eligible candidate is receiving Social Security retirement benefits. Ohio repealed its offset in 2007 with unanimous votes in both houses of the legislature. Ohio would be in the only state in the nation that deducts one dollar of unemployment benefits for each dollar of Social Security retirement received.

- Disqualify applicants for unemployment benefits for violating the terms of their employee handbook. The bill would make violation of minor handbook provisions a “just cause” for discharge resulting in disqualification from benefits regardless of the circumstances of the violation and without a showing of fault. Ohio would be the only state in the country with such a provision.

- Keep anyone from getting UC benefits who receives Social Security disability insurance payments for the same week. States already make an individualized inquiry into whether an applicant is available and able to work—a requirement to receive UC — despite claiming or receiving disability benefits. Given that individuals on disability are encouraged to work, those that are able to do so and then become involuntarily unemployed should not be automatically barred from UC. Minnesota is the only state we have found that explicitly says that Social Security disability payments can make you ineligible for UC.

Unemployment compensation does not just help families buy the essentials they need, and permit job seekers to look for work more effectively because they have money to put gas in the car and keep their Internet access. Unemployment benefits “allow the unemployed to maintain more of their previous consumption than they otherwise would be able to,” ODJFS noted in a filing last year. “When the unemployed cut back on spending, the business owners that serve them lose. By cushioning the fall in these families’ incomes, unemployment insurance not only helps the families that receive it, but also prevents further production cuts and layoffs.”

Thank you for allowing me to testify on this legislation. I am happy to answer any questions that you may have.

###

Policy Matters Ohio is a nonprofit, non-partisan research institute

with offices in Cleveland and Columbus.

Photo Gallery

1 of 22