Ohio foreclosures: Damage in the wake of housing crisis

November 04, 2016

Ohio foreclosures: Damage in the wake of housing crisis

November 04, 2016

Key Findings

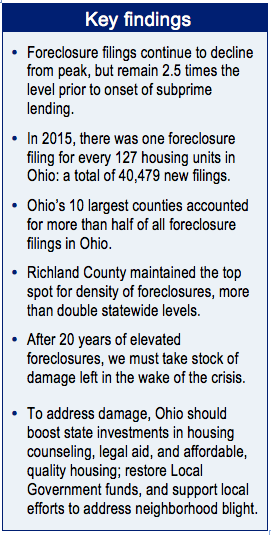

- Foreclosure filings continue to decline from peak, but remain 2.5 times the level prior to onset of subprime lending.

- In 2015, there was one foreclosure filing for every 127 housing units in Ohio: a total of 40,479 new filings.

- Ohio’s 10 largest counties accounted for more than half of all foreclosure filings in Ohio.

- Richland County maintained the top spot for density of foreclosures, more than double statewide levels.

- After 20 years of elevated foreclosures, we must take stock of damage left in the wake of the crisis.

- To address damage, Ohio should boost state investments in housing counseling, legal aid, and affordable, quality housing; restore Local Government funds, and support local efforts to address neighborhood blight.

Foreclosures continue to decline, but remain elevated; Ohio can do more to prevent them.

Executive Summary

In 2015, there were 40,479 new foreclosure filings in Ohio, amounting to one foreclosure filing for every 127 housing units. The number is less than half peak levels seen in 2009, and 7 percent lower than in 2014. However, the number remains 2.5 times higher than levels prior to the onset of sub-prime lending in the mid-1990s.

{kind=link}

Foreclosures in large counties declined faster than the statewide average but remain a substantial portion. More than half of 2015 foreclosure filings were in the state’s 10 largest counties (60 percent), but the number of foreclosure filings in these counties fell at a faster rate (9 percent lower than in 2014, compared with a 7 percent decline statewide). Filings in Franklin County declined 30 percent, Lucas 18 percent, and Stark 12 percent, compared to a 9.4 percent drop statewide. Filings increased in Summit and Mahoning counties.

Foreclosure density, by county, demonstrates community impact. For every 1,000 people in Ohio there were more than three foreclosure filings in 2015. The foreclosure density in Richland County was more than double the statewide level, with nearly eight foreclosures per 1,000 residents, giving it the top spot for a second straight year in a row. Eight counties from last year’s top 10 list remained. Jackson and Montgomery counties rejoined the list, replacing Franklin and Brown.

Addressing 20 years of foreclosures. Foreclosures began increasing 20 years ago, following the onset of sub-prime lending. After two decades of elevated foreclosures, now beginning to stabilize, it is time to assess the damage left in the wake of the crisis. The task is too big for this report, but we outline further steps the state can take to ameliorate negative impacts on families, neighborhoods, and local government. Since 1996, there have been more than 1 million foreclosure filings in Ohio. Not all filings result in foreclosure, but the sheer volume of filings provide insight into the severity of the problem in Ohio. To reduce foreclosure rates, ameliorate economic distress, and address blight, the state of Ohio should: 1) boost state funding levels for housing counseling and help fund legal aid; 2) restore the Local Government fund and increase state and local funding for affordable, quality housing; and, 3) provide flexible state support for local efforts to address neighborhood blight.

In 2015, Ohio foreclosure filings fell 7.4 percent from previous year

There were 40,479 new foreclosure case filings across Ohio in 2015, according to data collected by the Supreme Court of Ohio.[1] This equates to one foreclosure filing for every 127 housing units in the state.[2] It is 3,248 fewer filings than the 43,727 filings seen in 2014, and less than half 2009 record levels, when there were 89,000 foreclosure filings. That said, the number of annual foreclosures remains well above levels seen in the 1990s, prior to rapid growth of subprime lending and the onset of the housing crisis. Figure 1 below shows that while current foreclosure rates are down significantly from the high, they remain 2.5 times above the 1995 level, when 15,975 foreclosure cases were filed. The number of new foreclosure filings fell in 59 of the 88 Ohio counties last year, but remains at least double the 1995 rate in 73 counties.[3]

More than half Ohio’s 2015 foreclosure filings from 10 largest counties

In 2015, more than half of the state’s 40,479 foreclosure case filings occurred in Ohio’s 10 most populated counties (24,394). However, these 10 counties saw a faster decline in the number of foreclosure filings than the rest of the state, with 9.4 percent fewer filings than 2014, compared to a 7.4 percent decrease statewide.

Franklin County saw the largest drop in new filings from last year (30 percent), followed by Lucas, Stark and Cuyahoga. All four counties showed larger decline rates than the state as a whole. Rates in Hamilton, Butler and Montgomery also declined, but at slower speeds.

Two of Ohio’s largest counties - Summit and Mahoning - had continued increases in the number of cases filed. Summit County filings increased 21 percent, Mahoning 2 percent. The number of new Lorain County foreclosure case filings stayed the same.

Deep community impact

For every 1,000 people in Ohio, there were more than three (3.49) foreclosure filings in 2015. Richland County had about eight foreclosure filings for every 1,000 residents in 2015, the highest such rate in the state (7.84). This earned Richland the “top” spot for the second year in a row, and was a 24 percent increase from the 771 foreclosures filed the previous year.

Eight counties from last year’s top ten list remained on the list. Three of those counties had an increase in their filing rates: Coshocton, Summit and Trumbull. Summit County presented the most noticeable increase, 21 percent, with more than five foreclosure filings per 1,000 county residents.

Four of the eight counties - Cuyahoga, Mahoning, Erie and Ashtabula - showed declines in 2015. In Cuyahoga County, the number of filings for every 1,000 people decreased 8 percent to 5.14 per 1,000 people, the lowest level in more than a decade.

Montgomery and Jackson counties are new to the top 10 list this year, replacing Franklin and Brown counties, where filing rates fell by more than 27 percent.

Twenty years of foreclosures hurt families and communities across Ohio

While the number of annual foreclosure filings remains higher than levels seen in the mid-1990s, the foreclosure rate has begun to decline and level off from its peak in 2009, making it a good time to assess the damage from two decades of elevated foreclosures. In Ohio, the rate of foreclosure filings began to increase dramatically in 1996. Since then, there have been more than 1 million foreclosure filings across Ohio. While not every filing resulted in an actual foreclosure, the total number over the past two decades provides a hint as to the severity of the problem. Table 3 below shows the 10 counties in Ohio most affected over the past 20 years. Cuyahoga County was hit hardest with nearly 150 foreclosure filings for every 1,000 residents.

Foreclosure is a first step on the path to economic insecurity.

As a result of the housing crisis, a greater number of families are finding themselves in economic hardship. Losing a home leads to a decline in financial stability, credit scores and household net worth, while increasing the likelihood of filing for bankruptcy.[4] Homeless shelters have seen an increase in people served. Food assistance caseloads increased.[5] The intense stress of losing a home can even bring about ill health, domestic violence, suicide and increased calls to crisis hotlines.

The community and surrounding neighbors suffer as well.

A high density of foreclosures hurts property values and boosts crime, attracting squatters, vandals and drug users. [6] Prolonged periods of vacancy results in property deterioration and increased risk of fire.[7] Local governments in hard-hit communities often face serious fiscal stress. Municipalities must spend more on policing and fire suppression at abandoned properties, providing temporary assistance for displaced residents, and maintaining abandoned properties. These increased demands on local government come at a time when property tax revenues are plunging due to greater numbers of property tax delinquencies and lower property values.[8]

Table 4 shows Ohio counties that have appeared on our top 10 list over the years for having a high number of foreclosure filings per capita.

These communities may be more likely to face the fiscal distress noted above.

While Richland County has only been among the top ten since 2013, Cuyahoga has made the list every year since we started compiling this data in 2004 (12 years). Montgomery County has been on 10 of 12 top 10 lists, Lucas nine, Brown eight, Summit and Preble seven. Mahoning and Highland made half of the 12 top 10 lists (6).

Conclusion and Recommendations

Foreclosures represent a major blow against families’ biggest source of savings and financial stability. Foreclosed homes too often become vacant and abandoned, sapping vitality from communities. Once vacant they don't bring in property taxes, meaning communities have far fewer resources to deal with struggling families and troubled properties left behind. All of this creates a downward spiral. Much important work already has been done to cope with a decade and a half of elevated foreclosures. Here, we recommend additional steps to reduce Ohio’s foreclosure rates and battle the blight and economic distress foreclosures cause.

Boost state investment in housing counseling. Foreclosure usually happens when people can’t make their house payments and can’t sell their home because it is no longer worth the amount owed on their mortgage. The Ohio Housing Finance Agency estimates more than 10 percent of Ohio homeowners are in this position, dubbed “under water.”[9] Housing counselors guide homeowners through the complex loan restructuring process to avoid foreclosure. Housing counseling programs, such as the federally funded NeighborWorks program, are not everywhere in Ohio. Existing housing counseling infrastructure should be strengthened and expanded.

Provide state funding for Legal Aid. Those without financial resources can benefit from assistance to navigate legal difficulties in the foreclosure process. Legal Aid services, which can help, need more resources. Since the Great Recession, Ohio’s Legal Aid services have lost roughly a quarter of their statewide funding, forcing major staff reductions. The upcoming budget should appropriate money to restore Ohio’s Legal Aid to pre-recession funding levels.

Restore local government funding. Local governments are currently working with $1 billion less in 2017 than they had in 2010 (when adjusted for inflation) due to cuts in state aid and elimination of local tax sources. To enable communities to address increased needs and restore the physical blight created in the past two decades, the state should:

- Restore revenue sharing through the local government fund, which has been cut in half (hurting cities, villages, townships and counties).

- Reinstate an estate tax on Ohio’s wealthiest estates - those over $1 million in value - and direct the revenues to local government entities. In the past, this money was used to pay capital costs of police fleets and fire trucks, taking pressure off a community’s general fund.

Dramatically increase state and local resources for quality, affordable housing. In 1991, Ohio voters approved a constitutional amendment designating housing as a public purpose. The Ohio Housing Trust Fund was established as the primary way to invest in needs for affordable housing and assist homeless people. The fund has been supported since 2003 by a fee that mirrors the county recordation fee. Unfortunately, the size of the fund continues to decline - from $53 million in fiscal year 2013 to $42 million in the current 2017 fiscal year - at a time when far more resources are needed, not less.

In some communities, the Ohio Housing Trust Fund is matched and leveraged by a local housing trust fund. In Franklin County, a local Affordable Housing Trust leverages private and public resources for investments in rental housing, supportive housing and home ownership. The Affordable Housing Trust uses financing tools to raise market values, stimulate private development, and contribute to revitalization on a neighborhood level. These local trust funds should be replicated in other communities to supplement and leverage the Ohio Housing Trust Fund. The state of Ohio should play a key role in helping make that happen.

Increasing state and local resources would assist low-income homebuyers, counsel families facing foreclosure and expand permanent housing for homeless people, emergency home repair, handicapped accessibility modifications and other affordable housing investments. They would also enable housing rehabilitation and home weatherization to reduce utility costs.

Provide flexible state support for local efforts to address neighborhood blight. Federal dollars from the U.S. Treasury’s Hardest Hit fund are used to stabilize property values by removing and greening vacant and blighted properties to help prevent future foreclosures. Additional state investment could enable existing land banks and housing development entities to expand on the good work being done to restore neighborhoods. Additional resources, flexible in nature, could be used not only for targeted demolition but also housing rehabilitation, depending on which is more appropriate for a property and a neighborhood. In less viable neighborhoods, where few remaining homeowners feel stuck amongst dense clusters of abandoned properties, relocation assistance may be a useful tool in a creative community toolbox.

Ohio has great neighborhoods, beautiful houses, and dedicated community groups working to ensure that our residents have safe, affordable places to live. Two decades of elevated foreclosures have taken their toll on our families and communities. As the crisis begins to ease, now is the time for assertive policy to restore our neighborhoods so that the next generation can build wealth and thrive with the stability that safe housing provides

Footnotes

[1] Ohio Supreme Court, Policy Matters Ohio review of filings in U.S. district courts. Numbers include both tax and mortgage foreclosures, but not tax foreclosure filings at county boards of revision for vacant abandoned properties.

[2] Housing units from U.S. Census Bureau at http://factfinder.census.gov/faces/tableservices/jsf/pages/productview.xhtml?src=CF

[3] There were 24 counties with increases in foreclosure filings. Among those counties where the number of filings remained unchanged are: Harrison, Hocking, Huron, Lorain and Morgan.

[4] Kingsley, Smith & Price, The Urban Institute, The Impacts of Foreclosures on Families and Communities (2009)

[5] Measures of State Economic Distress: Housing Foreclosures and Changes in Unemployment and Food Stamp Participation. See also Elmer & Seelig, Insolvency and Trigger Events in the Theory of Single-Family Mortgage Default (FDIC Working Paper, 1998).

[6] Kingsley, Smith & Price, The Urban Institute, The Impacts of Foreclosures on Families and Communities (2009). See also Bess, Assessing the Impact of Home Foreclosures in Charlotte Neighborhoods, Geography and Public Safety (2008), and Immergluck & Smith, The Impact of Single-Family Mortgage Foreclosures on Neighborhood Crime, Housing Studies (2006).

[7] Immergluck & Smith, The External Cost of Foreclosure: The Impact of Single-Family Mortgage Foreclosures on Property Values, Housing Policy Debate (2006).

[8] Pagano & Hoen, City Fiscal Condition in 2008, National League of Cities (2008).

[9] Ohio Housing Finance Agency, Ohio Housing Needs Assessment: Technical Supplement to the Fiscal Year 2017 Annual Plan (2016).

Photo Gallery

1 of 22